India Car Sales Report April 2026 The Indian automotive landscape in has presented a fascinating study in market resilience and shifting consumer preferences. Following the traditional high-octane finish of the financial year in March, the Passenger Vehicle (PV) retail market experienced a widely anticipated sequential cooling off. However, beneath the surface of the headline numbers lies a story of established giants holding their ground and aggressive new entrants making significant inroads.

The April 2026 Retail Overview: A Seasonal Shift

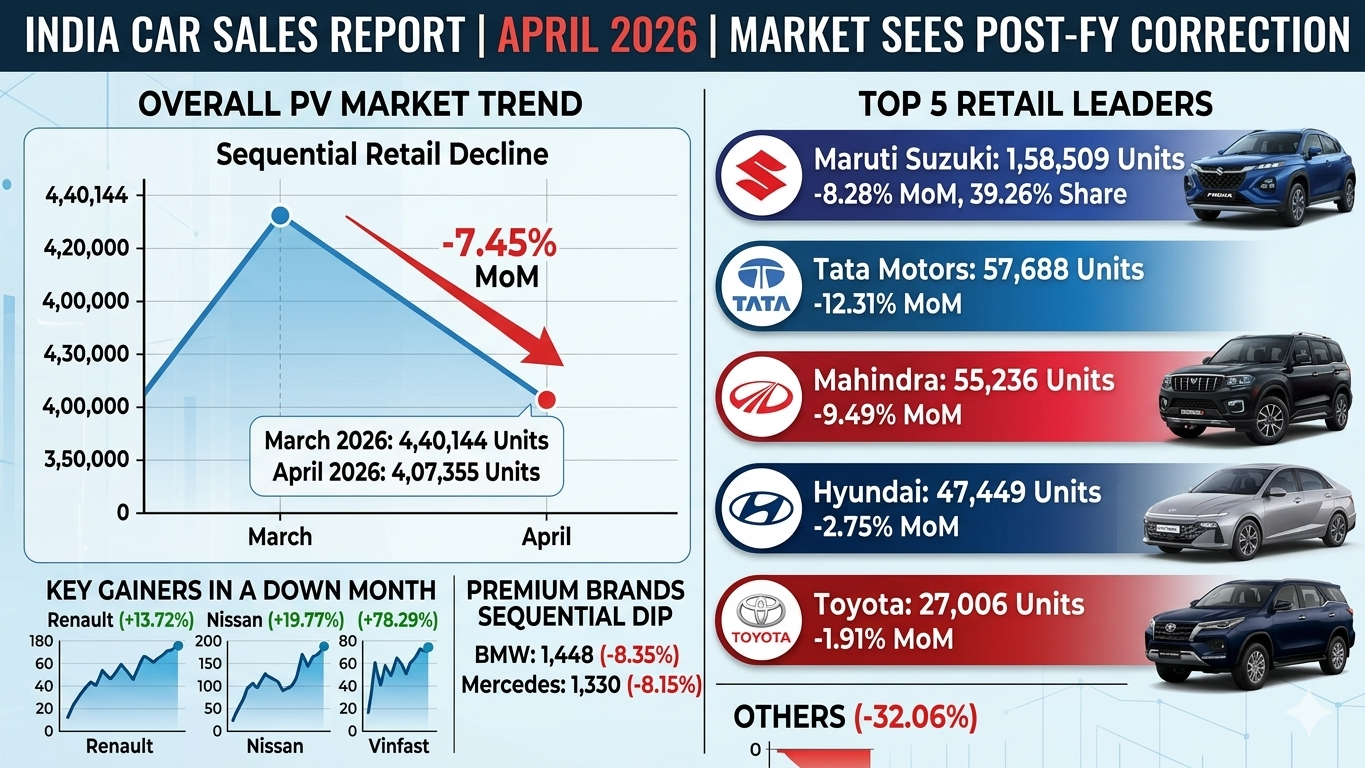

Total PV retail sales for April 2026 stood at 4,07,355 units. This represents a 7.45% decline compared to the 4,40,144 units moved in March 2026. While a “red” month might concern casual observers, industry veterans recognize this as a standard “post-March hangover.” Dealers typically push massive inventories and aggressive discounts in March to meet annual targets, making April a period of stabilization and inventory correction.

Despite the overall dip, the market remains robust compared to historical trends, with several brands demonstrating that product freshness can overcome seasonal slumps.

India Car Sales Report April 2026 : Maruti Suzuki Leads the Pack

Maruti Suzuki continues to be the undisputed “Big Brother” of the Indian roads. With 1,58,509 units retailed in April, it commanded a staggering 39.26% market share. Although its sales dipped by 8.28% from March’s high of 1,72,814 units, the sheer volume Maruti moves remains the benchmark for the industry.

| Rank | Brand | April 2026 Sales | March 2026 Sales | MoM Change |

| 1 | Maruti Suzuki | 1,58,509 | 1,72,814 | -8.28% |

| 2 | Tata Motors | 57,688 | 65,784 | -12.31% |

| 3 | Mahindra | 55,236 | 61,029 | -9.49% |

| 4 | Hyundai | 47,449 | 48,791 | -2.75% |

| 5 | Toyota | 27,006 | 27,533 | -1.91% |

Tata Motors and Mahindra locked in a tight battle for the second and third spots. Tata retailed 57,688 units, seeing a double-digit decline of 12.31%, likely due to a high base in March. Mahindra followed closely with 55,236 units. Notably, Hyundai showed incredible stability, posting the smallest decline among the top five brands at just 2.75%, proving that their current portfolio has consistent demand regardless of the month.

The “Trend-Buckers”: Who Grew in a Down Month?

While the giants saw declines, a handful of brands managed to swim against the current. These gains are primarily attributed to new launches and the increasing adoption of electric vehicles.

Renault (+13.72%): The French automaker retailed 4,087 units. This growth was fueled by the refreshed Triber and the significant buzz surrounding the new Duster, which has finally started gaining volume momentum.

Nissan (+19.77%): Moving 3,047 units, Nissan’s growth is almost entirely credited to the new Gravite compact MPV, which seems to have hit a sweet spot with Indian families looking for value and space.

Vinfast (+78.29%): The most shocking performer of the month. The Vietnamese EV specialist jumped from 691 units in March to 1,232 units in April. This suggests that their localized strategy and EV infrastructure investments are beginning to pay off.

Skoda & Volkswagen (+1.69%): The German-Czech alliance retailed 8,913 units, showing that the premium “driver-focused” segment remains insulated from mass-market fluctuations.

Luxury and Niche Brands

The luxury segment mirrored the mass market’s downward trend. BMW led the premium charts with 1,448 units, slightly ahead of Mercedes-Benz at 1,330 units. Both saw an ~8% decline.

On the other hand, BYD (469 units) and JLR (450 units) saw modest gains, indicating that the very top end of the market and the high-end EV space are operating on a different cycle than the volume players.

Future Outlook: What to Expect in May and Beyond

The April 2026 data suggests that while the “pent-up demand” era might be cooling, the market is shifting toward feature-rich SUVs and reliable EVs. For the remainder of the quarter, we expect:

Increased Competition in Compact MPVs: With Nissan and Renault seeing growth, expect Maruti and Kia to respond with new variants or aggressive financing.

The Rise of New Entrants: Vinfast’s surge is a wake-up call for domestic manufacturers to not take the EV transition lightly.

Inventory Normalization: By late May, the “March effect” will have completely worn off, and we will see a clearer picture of the true annual growth rate.

As we move further into 2026, the Indian consumer is clearly becoming more discerning, prioritizing safety, technology, and powertrain diversity over brand loyalty alone.