The early months of 2026 have made one thing clear: the industrial engine of Asia is running on high-octane technology. A massive industrial profit surge is sweeping through the region’s top economies, rewriting the rules of global manufacturing. On Wednesday, fresh data from China’s National Bureau of Statistics (NBS) sent ripples through international markets, revealing that Chinese industrial profits jumped by a staggering 18.2 percent year-on-year during the first four months of 2026. This performance marks a dramatic 2.7 percentage point acceleration from the first quarter, proving that Beijing’s proactive macroeconomic interventions are finally bearing fruit.

But China isn’t sprinting alone in this high-tech arena. Just across the border, India is leveraging its own domestic infrastructure boom, Performance Linked Incentive (PLI) schemes, and corporate earnings momentum to mount a highly competitive counter-offensive. While China relies heavily on global tech supply dominance and raw material recovery, India is finding its strength in domestic capital expenditure (capex), engineering, and a rapidly expanding ecosystem of medium- and high-technology industries.

To truly understand where global manufacturing is heading, we need to peel back the layers of this dual Asian expansion, evaluating how both giants are converting high-tech innovation into cold, hard corporate profits.

Highlight Of The Economic Analysis:

China’s Massive Profit Surge: Boosted by proactive government policies and price recoveries, China’s major industrial profits jumped 18.2% year-on-year in the first four months of 2026.

High-Tech Sector Dominance: High-tech manufacturing is driving China’s growth, highlighted by a 44.8% profit skyrocket in tech fields and a massive 601.7% surge in electronic special materials.

India’s Infrastructure-Led Growth: India is matching this momentum with strong domestic spending and engineering demand, leading to record-breaking annual performances for heavy machinery and power sectors.

Shared “Uneven” Recovery: Both nations face a sector divide; while high-tech fields boom, China’s real estate supply chains and India’s small-to-medium enterprises (MSMEs) still face severe margin pressures.

The Path Forward: The data confirms that both economic giants are shifting away from low-cost assembly to master advanced engineering, semiconductors, and artificial intelligence.

Understanding China’s Tech-Driven Profit Explosion

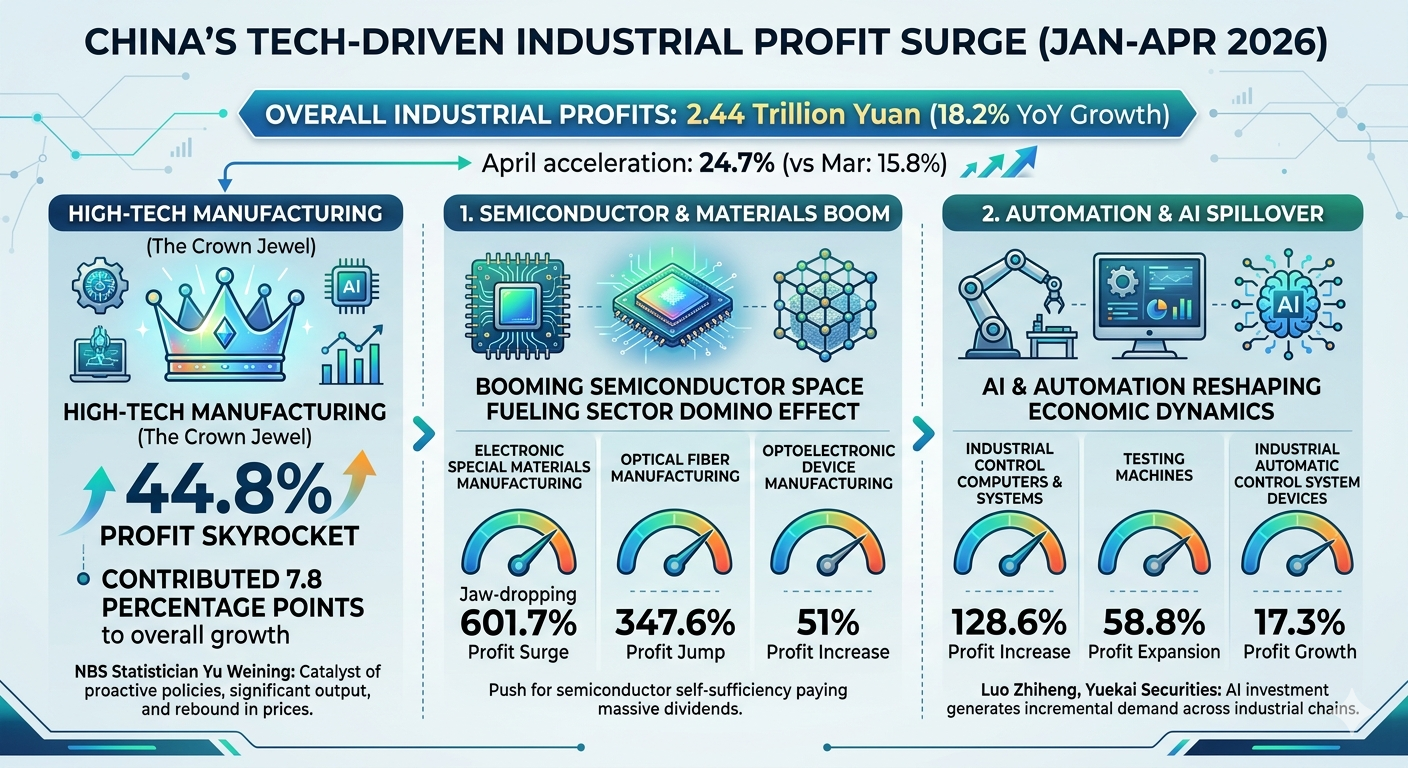

According to the NBS, Chinese industrial enterprises with an annual main business revenue of at least 20 million yuan ($2.95 million) saw their total profits climb to 2.44 trillion yuan in the January–April window. In April alone, the acceleration was even more blinding, with major industrial firms posting a 24.7 percent year-on-year increase in profits compared to March’s 15.8 percent growth.

NBS statistician Yu Weining pointed directly to the catalyst: a mix of proactive macroeconomic policies, significant industrial output expansion, and a strong rebound in factory-gate pricing.

However, the real crown jewel of this recovery is the high-tech manufacturing segment. Profits in high-tech manufacturing skyrocketed by 44.8 percent during the first four months, single-handedly contributing 7.8 percentage points to the country’s overall industrial bottom line.

1. The Semiconductor and Material Boom

A deeper look into China’s industrial sectors highlights a booming semiconductor space that has ignited a domino effect across upstream and midstream segments:

Electronic Special Materials Manufacturing: Earnings skyrocketed by a jaw-dropping 601.7 percent.

Optical Fiber Manufacturing: Profits surged by 347.6 percent.

Optoelectronic Device Manufacturing: The sector marked a solid 51 percent profit jump.

This explosive growth shows that China’s multi-year push for semiconductor self-sufficiency is paying massive financial dividends as global tech supply chains formalize around localized nodes.

2. Automation and Artificial Intelligence Spillover

The rapid integration of Artificial Intelligence (AI) and industrial automation has shifted from a theoretical trend to a concrete driver of corporate balance sheets. Manufacturers of industrial control computers and systems saw a profit increase of 128.6 percent. Testing machines expanded by 58.8 percent, while industrial automatic control system devices grew by 17.3 percent.

Luo Zhiheng, chief economist at Yuekai Securities, pointed out that the rapid development of AI is reshaping China’s economic dynamics. The investment in AI infrastructure is generating incremental demand across entire industrial chains, manifesting as stronger pricing power for computing power products, upstream materials, and electronic equipment.

How India Compares: The Power of Domestic Capex and Structural Shifts

While China builds on its massive global export machinery and localized chip production, India’s industrial strategy in early 2026 tells a story of domestic resilience, structural formalization, and engineering depth.

India entered 2026 as one of the world’s fastest-growing industrial economies. Data from the Union Budget and mid-quarter indicators reveal that India’s manufacturing Gross Value Added (GVA) expanded at a robust clip (averaging over 7.5% to 9% in recent quarters). According to the Ministry of Commerce and economic trackers, medium- and high-technology industries now contribute a substantial 46.3 percent of India’s total manufacturing value added.

Rather than relying purely on external electronics demand, India’s corporate profit trajectory in early 2026 is anchored by a persistent domestic infrastructure spending cycle and an aggressive push into high-end engineering.

1. Heavy Engineering and Power Sector Outperformance

Reflecting India’s industrial strength, corporate giants have posted record-breaking figures for the financial year ending in the spring of 2026. For instance, Cummins India—a bellwether for the industrial capex and power generation cycle—reported its strongest-ever annual financial performance in May 2026. Total sales surged 18% year-on-year to ₹11,950 crore, with domestic sales jumping 19%.

What makes India’s corporate earnings compelling is the expansion of operating leverage. Industrial profit growth is regularly outpacing revenue growth due to cost optimization and a stable domestic pricing environment. Cummins’ profit before tax jumped 24% to ₹3,104 crore, matching the resilient demand for heavy machinery, data center power backups, and infrastructure solutions across the country.

2. The Rising Wave of Specialized Components and Electronics

India is gradually attempting to mirror China’s component success through its PLI frameworks, which target electronics, advanced chemistry cells, and automotive components. Heavy equipment and specialized engineering players like Carraro India reported a massive 76 percent surge in profit after tax (PAT) for the final quarter of the fiscal cycle, driven by domestic agricultural upgrades (such as 4WD tractors following GST restructurings) and a 31% expansion in construction equipment demand.

Simultaneously, India’s technology infrastructure arms, such as Essar’s Black Box Limited, closed their seasonal books with order books crossing the $1 billion mark (~₹7,000 crore), a 57% year-on-year increase. This shows that Indian enterprise demand for digital infrastructure, data center construction, and smart network integration is booming in perfect tandem with the broader global AI migration.

3. Raw Materials and Upstream Processing

Just as China experienced an 88.1 percent surge in raw material manufacturing profits, India’s core sectors have kept pace. Major metals and mining conglomerates, such as Hindalco Industries, reported all-time high consolidated revenues and EBITDA for their domestic businesses in late May 2026. Driven by strong operational efficiencies and copper business expansions, India’s upstream sector is directly fueling the physical infrastructure needed for high-tech manufacturing.

Side-by-Side: China vs. India Industrial Landscape (Early 2026)

| Metric / Focus Area | China’s Industrial Sector | India’s Industrial Sector |

| Headline Profit Growth | 18.2% YoY increase (Jan-Apr 2026); April alone hit 24.7%. | High-single to double-digit GVA growth; individual engineering/tech firms reporting 20-40% profit spikes. |

| Primary Growth Drivers | Semiconductors (+601% special materials), Industrial Automation (+128%), AI spillover, and Raw Materials (+88.1%). | Infrastructure capex, Power Generation systems, Data Center infrastructure, and Automotive/Agri-engineering. |

| Policy Catalysts | Proactive macroeconomic stimulus, supply-side capacity management, and price recovery measures. | Union Budget targeted manufacturing incentives, PLI scheme execution, and aggressive infrastructure funding. |

| Market Sentiment | Shanghai Composite (+5.7%) and Shenzhen Component (+12.1%) surged in April 2026 reflecting a cyclical recovery. | Domestic stock markets hit repeated record highs, driven by consistent institutional capex investments. |

| Core Structural Challenges | Persistent margin pressures in downstream traditional processing, consumer goods, and property-linked sectors. | Moderate global export headwinds slowing down job creation in traditional texturing/textile sectors. |

The Shared Challenge: Divergence and the Downstream Pinch

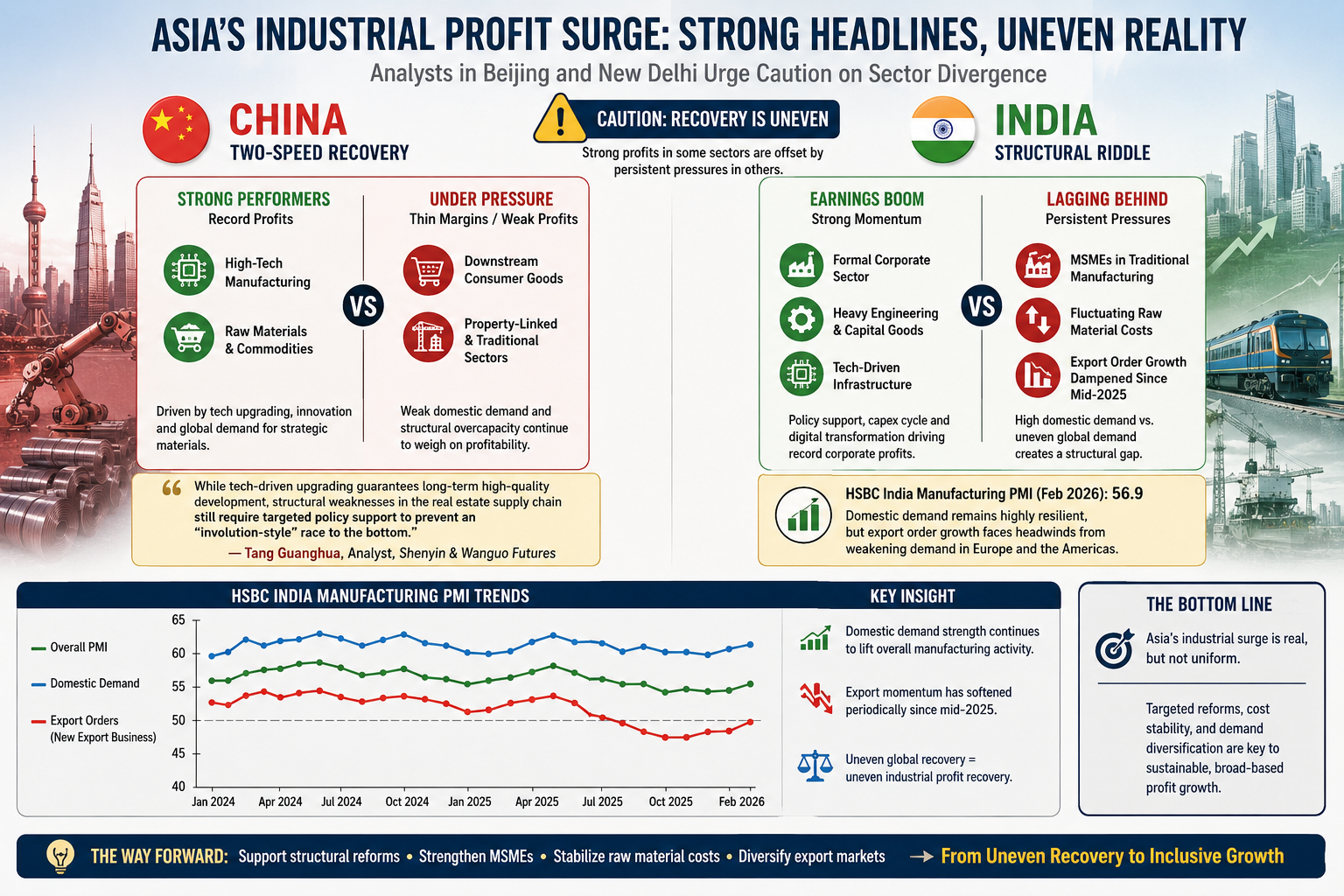

Despite the optimistic headlines surrounding the global industrial profit surge, analysts in both Beijing and New Delhi urge caution regarding sector divergence. The economic recovery across Asia is undeniably uneven.

In China, while high-tech and raw materials segments are raking in record profits, downstream consumer goods and traditional property-linked sectors continue to operate under thin margins. Tang Guanghua, an analyst at Shenyin & Wanguo Futures, emphasizes that while tech-driven upgrading guarantees long-term high-quality development, structural weaknesses in the real estate supply chain still require targeted policy support to prevent an “involution-style” race to the bottom.

India faces a comparable structural riddle. While the formal corporate sector, heavy engineering, and tech-driven infrastructure are witnessing an unprecedented earnings boom, small and medium enterprises (MSMEs) in traditional downstream manufacturing face lingering pressures from fluctuating raw material costs. Furthermore, as HSBC India’s Manufacturing PMI data from early 2026 points out, while domestic demand remains highly resilient (pushing the PMI to a strong 56.9 in February), export order growth has seen periodic dampening since mid-2025 due to uneven purchasing power in Europe and the Americas.

Looking Ahead: Can the Momentum Sustained?

The industrial data from the first four months of 2026 proves that both China and India are successfully pivoting toward a high-value, technology-first manufacturing blueprint.

China’s ability to generate a 44.8% profit jump in high-tech manufacturing signals that its factory floors are no longer just about low-cost assembly; they are now the epicenter of automated, intelligent global supply networks. Lynn Song, chief economist for China at ING, notes that the current trajectory points toward the first full-year increase in Chinese industrial profits since 2022, signaling a definitive end to the post-pandemic stagnation.

India, on the other hand, is building an industrial fortress rooted in internal consumption and structural modernization. By funneling massive capital into power grids, digital infrastructure, and localized component manufacturing, India is insulating its industrial ecosystem from external shocks while preparing its corporate sector to capture shifting global supply chains.

For global investors and policy makers, the takeaway is clear. The economic narrative of 2026 is not about a slow, generalized recovery. It is about a high-velocity, tech-driven industrial profit surge where the nations that command semiconductors, artificial intelligence, and advanced engineering will ultimately dictate the wealth of tomorrow.