On Friday, May 29, 2026, Asian Paints Q4 Results shared its financial results for the final quarter of the fiscal year (Q4 FY26), and the numbers were excellent.

Showing why it is the biggest paint company in India, its net profit jumped by a massive 69% compared to the same time last year. This growth was driven by high customer demand, cheaper raw materials, and strong business operations.

Even with global economic and political challenges, the company performed incredibly well. To celebrate this success, Asian Paints also announced a large final dividend payout for its shareholders.

The Big Picture: Unpacking the Mind-Boggling Q4 Financial Matrix

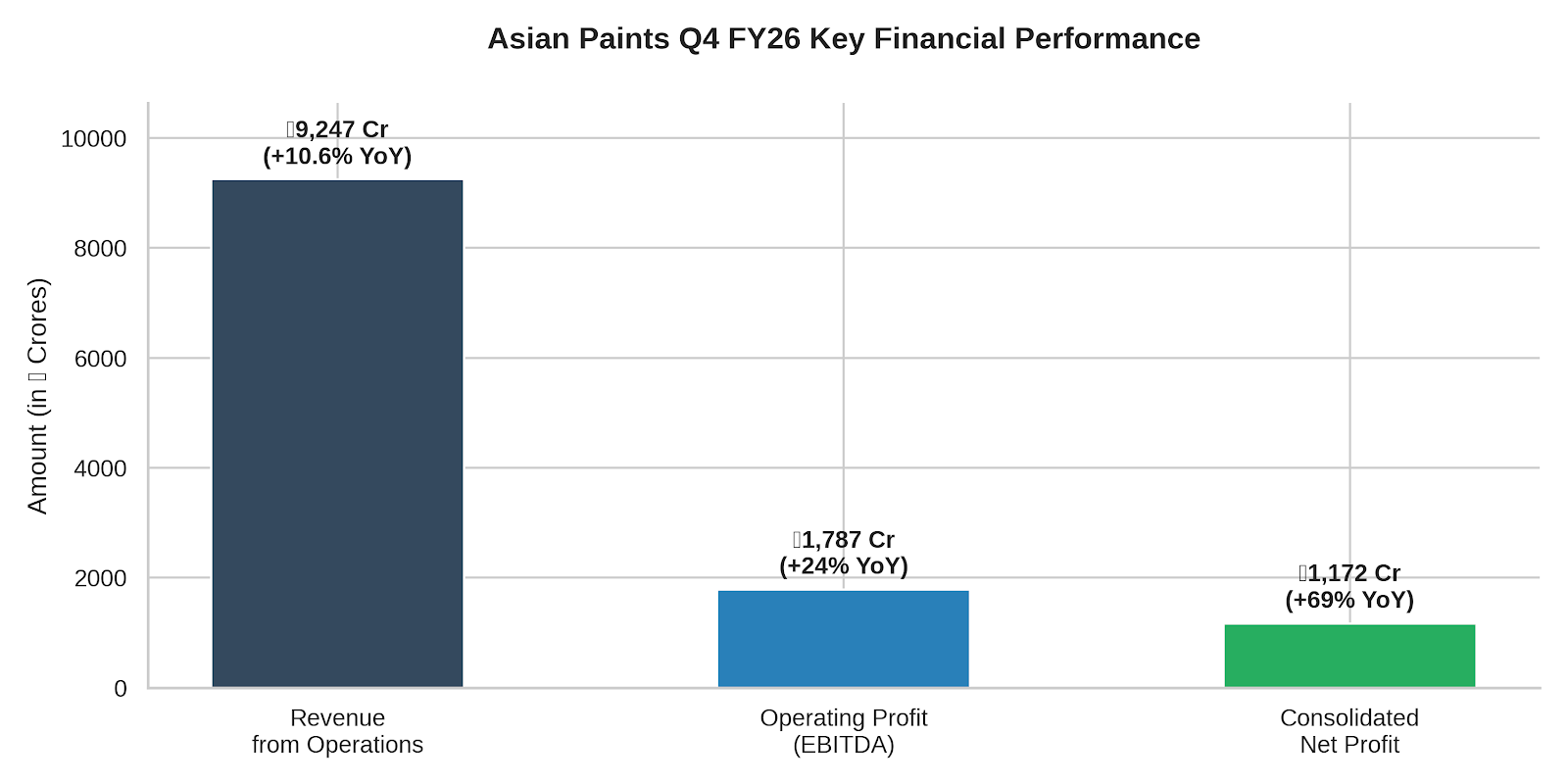

When you look beneath the surface of the headline figures, the sheer operational scale of Asian Paints becomes immediately evident. During the January-to-March quarter of 2026, the company’s consolidated net profit skyrocketed to an astonishing ₹1,172 crore. To put this performance into perspective, the company reported a net profit of ₹692 crore in the corresponding quarter of the previous fiscal year (Q4 FY25). This massive jump of 69% highlights a structural improvement in profitability that few market analysts had fully priced in before the announcement.

Here are the operational and dividend metrics that explain the rest of the company’s blockbuster performance:

EBITDA Margin Expansion: Jumped to 19.3% (up from 17.2% in Q4 FY25), showing much better control over raw material costs.

Strong Volume Growth: The core domestic business saw a solid 12.4% growth in decorative paint volume in India.

Shareholder Rewards: The board declared a total dividend of Rs. 27.50 per share (with a face value of Rs. 1) for the full fiscal year.

On the top-line front, revenue from operations registered a double-digit expansion, climbing 10.6% on a year-on-year basis to hit ₹9,247 crore. In the fourth quarter of the prior year, revenue sat comfortably at ₹8,359 crore. Crossing the ₹9,200 crore milestone in a single quarter underscores the broad-based consumption trends driving the Indian home decor and infrastructure boom.

EBITDA and Margin Expansion: The Real Story of Efficiency

While revenue growth indicates strong consumer demand, the true metric of operational excellence lies in the company’s profitability margins. Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) surged forward by 24% to settle at ₹1,787 crore, compared to ₹1,436 crore recorded in the same period last year.

More importantly, the consolidated EBITDA margin expanded significantly to 19.3%, up from 17.2% in Q4 FY25. This 210-basis-point expansion is a remarkable achievement for a manufacturing giant of this size. It proves that Asian Paints did not simply sell more paint; it managed its input procurement, supply chains, and manufacturing processes with extreme precision, capturing maximum profitability from every drop of paint shipped across its vast distribution network.

Shareholder Wealth Creation: The FY26 Dividend Bonanza ExplainedFor long-term investors, the announcement of the Asian Paints Q4 results brings a highly rewarding financial windfall. The board of directors has officially recommended a massive final dividend of ₹23 per equity share of face value ₹1 for the financial year ended March 31, 2026.

This premium payout is set to be presented for formal shareholder ratification at the company’s upcoming Annual General Meeting (AGM). However, the financial rewards do not stop there. When you combine this recommended final dividend with the interim dividend of ₹4.50 per share that was declared and paid to shareholders back in November 2025, the total dividend for the entire FY26 financial year reaches an impressive ₹27.50 per equity share.

Crucial Calendar Dates for Investors

To ensure you don’t miss out on this lucrative corporate action, it is vital to keep track of the official timelines established by the company’s management:

The Record Date: Asian Paints has designated June 23, 2026, as the official record date. This means that anyone holding the stock in their demat accounts by the close of business on this day will be legally entitled to receive the final dividend payout.

The Payment Date: Upon receiving the formal green light from shareholders during the AGM, the company plans to distribute the funds on or immediately after July 13, 2026.

This aggressive dividend distribution philosophy highlights the company’s strong free cash flow position. Even while investing heavily back into expanding its production capacities and acquiring emerging brands, Asian Paints continues to prioritize rewarding its core investor base.

Segment Performance Breakdown: What’s Driving the Momentum?

The phenomenal numbers reported in the final quarter were not accidental flash-in-the-pan events. They are the direct result of synchronized, high-octane growth across multiple business verticals, led primarily by the powerhouse domestic decorative coatings business.

1. The Indian Decorative Business: The Unstoppable Engine

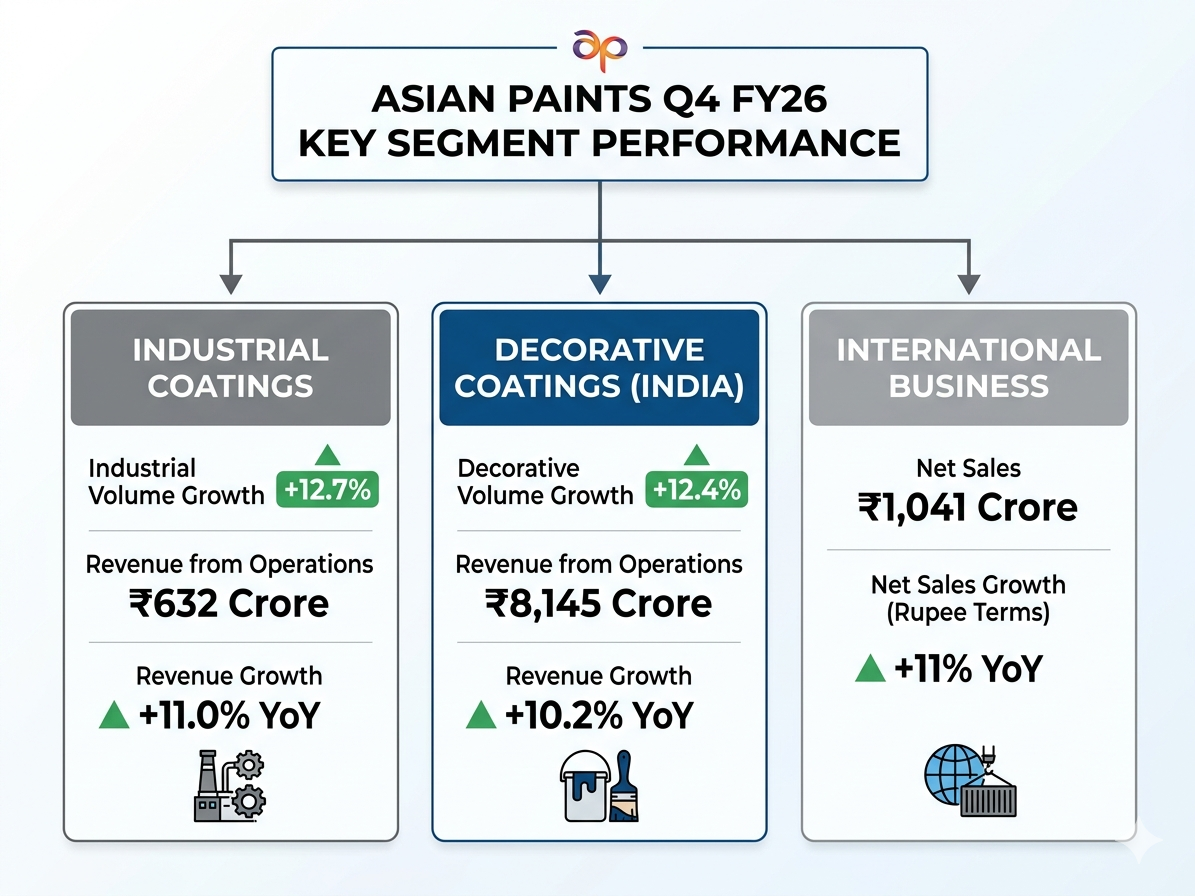

The home improvement and real estate decoration market within India remains the crown jewel of the company’s commercial operations. During Q4 FY26, this domestic segment recorded a stellar 12.4% volume growth alongside a solid 10.2% value growth.

This double-digit volume expansion signals that middle-class households, commercial developers, and mass-market consumers are actively upgrading their properties. The minor variance between volume and value growth points to strategic pricing calibrations and product-mix alterations implemented by Asian Paints to counter local competition while keeping their product lineup highly accessible to the average consumer.

2. Industrial Coatings: Accelerating Commercial Infrastructure

As the broader Indian economy expands, heavy infrastructure, manufacturing setups, and automotive lines require high-performance industrial coatings. This segment proved to be an excellent growth multiplier for Asian Paints during the quarter.

The robust demand trends in industrial coatings pushed the company’s combined domestic coatings performance to a remarkable 12.7% volume growth and an 11.0% value growth. By capitalizing on the government’s sustained infrastructure push, the industrial division has evolved into a highly reliable secondary revenue stream that reduces the company’s reliance on purely seasonal festive painting cycles.

3. International Operations: Overcoming Global Storms

Navigating cross-border commerce has been exceptionally challenging for global conglomerates over the past year. Despite these headwinds, the international business division of Asian Paints delivered an admirable performance, reporting an 11% increase in net sales when measured in Indian Rupee terms.

When adjusted for local foreign exchange variances—known as constant currency terms—the international sales growth stood at a healthy 8.2%. What stood out most in the international report cards was a marked improvement in localized profitability margins, achieved by shifting focus to high-margin premium products and restructuring supply logistics within key overseas markets in Asia, Africa, and the Middle East.

From the CEO’s Desk: Navigating Macroeconomic Realities

Reflecting on the blowout earnings report, Amit Syngle, the Managing Director & Chief Executive Officer of Asian Paints, shared deep operational insights into what made this quarter such an all-round success story.

“Q4 FY26 performance was a quarter of all-round performance, with double-digit volume and value growth and margin expansion. At an overall business level, margins improved through cost discipline aided by material deflation and operational efficiencies even as we continued to invest in long-term growth drivers.”

Syngle’s commentary highlights a fundamental truth about the modern corporate landscape: growth cannot survive on volume alone; it requires relentless cost management. By taking advantage of global material deflation—specifically lower crude oil derivative prices, which form the baseline chemical inputs for paint manufacturing—and pairing it with advanced automation and operational efficiency, Asian Paints successfully protected and expanded its fiscal boundaries.

Addressing the Geopolitical Elephant in the Room

However, corporate leadership is staying realistic about potential challenges ahead. Amit Syngle explicitly acknowledged that the broader external environment continues to be highly volatile. He pointed out that the ongoing West Asia conflict remains a primary source of near-term demand uncertainty and supply chain anxiety globally.

Fluctuations in international shipping routes, changing insurance premiums for freight, and volatile energy costs present continuous risks to corporate bottom lines. Despite these external pressures, Syngle expressed absolute confidence in the institutional durability of Asian Paints, noting that the company’s deep market roots, robust fundamental pillars, and strict execution strategies will allow it to handle upcoming volatility while sustaining a premium performance profile.

Stock Market Reaction: How Dalal Street Welcomed the NewsFor an equity market that had been eagerly awaiting concrete corporate earnings direction, the Asian Paints Q4 results provided a breath of fresh air. Immediately following the midday earnings release on Friday, May 29, the stock experienced a healthy influx of buying interest on the national bourses.

On the National Stock Exchange (NSE), shares of Asian Paints climbed upward to trade at ₹2,694.80 apiece, marking a steady single-day gain of 0.86%. Market analysts suggest that while the numbers are undeniably fantastic, the stock price reaction remained measured because long-term institutional fund managers are carefully evaluating how incoming monsoon patterns and global oil pricing structures might affect the company’s profit margins in the upcoming Q1 FY27 cycle.

Nevertheless, the positive market closing confirms that Dalal Street views the company as a safe, highly resilient pick capable of generating defensive growth even during broader market consolidations.

Analytical Deep Dive: The Secrets Behind the 69% Profit Surge

To truly understand how a mature corporation achieves a 69% explosion in net profit, we have to look past the surface-level numbers. This massive financial leap is built on a foundation of three distinct operational advantages:

THE THREE PILLARS OF PROFIT GROWTH . Input Cost Deflation (Cheaper crude oil derivatives & raw materials) . Premiumization Shift (Consumers moving toward high-end luxury finishes) . Distribution Mastery (Direct-to-dealer network bypassing middlemen)

1. Capitalizing on Crucial Input Cost Deflation

The paint industry is highly dependent on petrochemical inputs and titanium dioxide. When global commodity prices experience downward corrections, it creates a highly favorable environment for manufacturers. Asian Paints used this deflationary window perfectly. By securing long-term raw material contracts at lower rates, they successfully reduced their cost of goods sold (COGS), allowing a much larger percentage of each sales rupee to flow straight to the bottom line.

2. The Powerful Premiumization Phenomenon

There is an unmistakable shift happening across Indian real estate. Homeowners are no longer looking for basic whitewashing solutions; they are demanding luxury, weather-proof, anti-bacterial, and texturized premium finishes. Because Asian Paints has consistently invested in high-end brand sub-labels (such as Royale and Ultima), they captured the lion’s share of this high-margin market segment. Selling premium products naturally yields much higher margins compared to economy-grade products, significantly accelerating profit growth.

3. Unrivaled Logistics and Distribution Infrastructure

The company’s extensive distribution model is famously studied in global business schools. By bypassing traditional multi-layered distributor networks and supplying products directly to tens of thousands of retail dealers multiple times a day via an advanced supply chain system, Asian Paints keeps its inventory overhead incredibly low. This direct-to-retailer approach gives the company unmatched pricing flexibility and allows it to protect its market share from aggressive new industry entrants.

Forward Outlook: Can Asian Paints Maintain This Dominant Pace?

As we look ahead, investors are wondering if Asian Paints can keep up this great performance. Big new competitors are entering the market, but Asian Paints’ latest strong results show it is ready to fight for its top spot.

The company’s focus on expanding its services business—including specialized home waterproofing, interior design consultations, and modular kitchen solutions—positions it as an all-inclusive home decor ecosystem rather than just a basic paint manufacturer. This ecosystem approach builds deep customer loyalty, making it incredibly difficult for newer competitors to disrupt its market base.

While unpredictable geopolitical factors across West Asia and potential supply chain bottlenecks will require careful navigation, the company’s strong financial health, zero-debt profile, and exceptional distribution network provide an incredibly reliable safety net. For stakeholders who have watched the stock navigate multiple economic cycles over the decades, these Q4 results offer clear proof that Asian Paints possesses the strategic tools, corporate leadership, and execution capabilities required to sustain its long-term market dominance.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investors are advised to do their own research or consult with a certified financial advisor before making any investment decisions on the stock market.