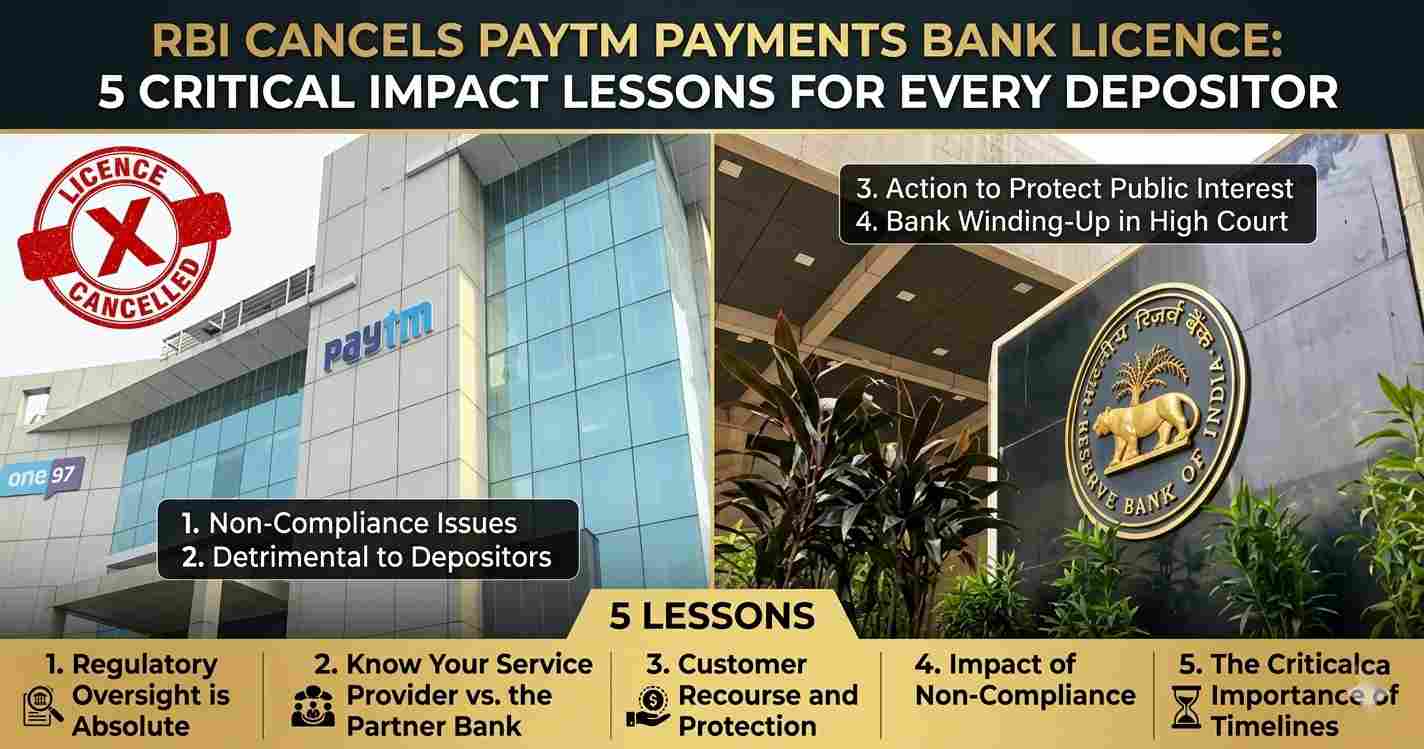

RBI Cancels Paytm Payments Bank Licence : The long-running regulatory battle between India’s central bank and one of its most prominent fintech experiments has reached its final chapter. On April 24, 2026, the Reserve Bank of India (RBI) officially cancelled the banking licence of Paytm Payments Bank Limited (PPBL). This decisive move marks the end of an era for the digital payments pioneer and sends a shockwave through the Indian financial ecosystem.

For millions of users who once relied on the “Paytm Karo” slogan for everything from tea stalls to highway tolls, the permanent closure of the bank wing is a sobering reminder of the supremacy of regulatory compliance over rapid growth.

RBI Cancels Paytm Payments Bank Licence:Why the Hammer Fell

The RBI’s notification was surgical and uncompromising. Citing Section 22 of the Banking Regulation Act, 1949, the regulator stated that the bank is no longer permitted to carry out any banking business. The reasons provided paint a picture of a management structure that consistently failed to align with the safety standards required of a financial institution.

1. Detrimental to Depositor Interest

The RBI explicitly stated that the affairs of PPBL were being conducted in a manner “detrimental to the interest of the bank and its depositors.” While the central bank did not detail the specific latest lapses in the final order, the history of the bank is riddled with concerns over KYC (Know Your Customer) irregularities and data privacy.

2. Management Credibility Gap

In perhaps the most stinging part of the statement, the RBI noted that the “general character of the management” was prejudicial to public interest. For a bank, trust is the primary currency. When the regulator loses faith in the leadership’s ability to follow the law, a licence cancellation becomes inevitable.

3. Persistent Non-Compliance

This wasn’t a sudden move. PPBL has been under the scanner since 2022. Despite multiple “last chances” and extensions, the bank failed to satisfy the conditions stipulated in its payments bank licence. The RBI concluded that no “useful purpose” would be served by allowing the entity to continue its operations.

What Happens to Your Money? The Winding-Up Process

If you still have funds in a Paytm Payments Bank account, a wallet, or a FASTag issued by the bank, the immediate question is: Is my money safe?

The RBI has offered a significant silver lining. According to the regulator, Paytm Payments Bank has enough liquidity to repay its entire deposit liability. Unlike cases of bank “failures” where assets are missing, PPBL simply isn’t allowed to function as a bank anymore.

The Road Ahead:

High Court Intervention: The RBI is moving an application before the High Court for the winding up of the bank.

Liquidator Appointment: A liquidator will likely be appointed to oversee the distribution of funds to depositors.

Withdrawals Only: While you can no longer deposit fresh money, the bank’s current mandate is strictly limited to facilitating withdrawals and clearing existing balances.

The “One97” Shield: Is the Paytm App Still Safe?

It is crucial to distinguish between Paytm Payments Bank (PPBL) and the Paytm App (One97 Communications Limited).

In a proactive filing to the Bombay Stock Exchange (BSE), One97 Communications clarified that it has distanced itself from the banking unit. Here is what users need to know about the services that ARE NOT affected:

Paytm UPI: Since Paytm transitioned to a multi-bank model (partnering with giants like Axis Bank, HDFC Bank, and SBI), your UPI handles ending in @ptsbi or @pthdfc will continue to work.

Merchant Services: The iconic Paytm Soundbox, QR codes, and Card Machines will remain operational as they are now powered by other partner banks.

Paytm Money & Gold: These subsidiaries operate under different licences (SEBI) and remain unaffected by the RBI’s action on the bank.

Timeline of a Tech Giant’s Regulatory Fall

The journey from being the poster child of India’s digital revolution to losing a banking licence was a slow-motion car crash.

| Date | Event | Impact |

| May 2017 | PPBL Launched | Promised to revolutionize banking for the unbanked. |

| March 2022 | Onboarding Ban | RBI stopped the bank from signing up new customers. |

| Jan-Feb 2024 | Deposit Freeze | RBI barred fresh deposits, top-ups, and wallet loads. |

| April 24, 2026 | Licence Cancelled | Official end of banking operations; winding up starts. |

5 Critical Lessons for the Modern Indian Investor

The downfall of PPBL offers a masterclass in the evolution of India’s “Fintech vs. RegTech” landscape.

1. Compliance is Non-Negotiable

In the tech world, the motto is often “move fast and break things.” In the banking world, if you break things, the regulator breaks you. PPBL’s struggle proves that no amount of venture capital or user base can substitute for a robust legal and compliance framework.

2. Diversify Your Digital Wallets

Never keep all your digital liquidity in a single basket. While the RBI ensures deposit insurance (up to ₹5 lakhs) and PPBL has the liquidity to pay back, the process of getting your money back during a winding-up can be time-consuming.

3. The “Payments Bank” Model is Challenging

Payments banks were designed for financial inclusion—they can’t lend money, only take deposits. With limited ways to earn interest and high costs of compliance, the business model itself is under pressure. This cancellation might trigger a consolidation in the remaining payments bank sector.

4. Read the Fine Print on “Partnerships”

Many users didn’t realize that their Paytm App was just a frontend for a bank. Understanding who actually holds your money—whether it’s a regulated scheduled commercial bank or a payments bank—is vital for long-term financial security.

5. Regulators are Watching the “Shadow” Management

The RBI’s comment on the “general character of management” suggests they are looking closely at how parent companies influence their banking subsidiaries. Transparency in corporate governance is now a top priority for the RBI.

Final Thoughts: The End of an Experiment

The cancellation of the Paytm Payments Bank licence is a “watershed moment” for Indian Fintech. It signals that the RBI will not hesitate to pull the plug on even the biggest players if they threaten the stability of the financial system.

For Vijay Shekhar Sharma and One97 Communications, the focus now shifts entirely to being a third-party app provider. For the rest of us, it’s a reminder that while digital convenience is great, the “boring” safety of regulatory compliance is what actually keeps our money secure.

What should you do now? If you have a balance in PPBL, initiate a transfer to another bank account immediately. Don’t wait for the court-ordered winding-up process to begin, as administrative delays are common in legal liquidations.

The Paytm App lives on, but the “Paytm Bank” is officially history.