On May 29, 2026, the Reserve Bank of India (RBI) released its latest annual report. The main takeaway is that Indian Economy is strong enough to handle big global challenges.

Even though there is an ongoing war in West Asia (the Middle East), rising shipping costs, rocky stock markets, and unpredictable weather, the RBI expects India’s economy to grow by 6.9% in the coming year (2026-27).

Why India is Doing Well:

People are buying: Local demand for goods and services inside India is very high.

Government spending: The government is putting a lot of money into building infrastructure like roads and public projects.

Healthy banks and businesses: Indian banks and companies have very clean financial records and low debt.

Risks to Watch Out For:

The RBI did warn about two main dangers that could slow things down:

The Middle East Conflict: If the war drags on, it could drive up global fuel prices.

Bad Monsoon Weather: A possible El Niño weather pattern might bring less rain this summer, which could hurt farming and cause food prices to rise.

1. The Global Economic Canvas: Dragged Down by Geopolitical Strains

GLOBAL ECONOMIC SHIFT (2026 FORECASTS) ┌──────────────────────────────┬──────────────────────────────┐ │ GLOBAL GDP GROWTH │ GLOBAL INFLATION │ ├──────────────┬───────────────┼──────────────┬───────────────┤ │ Old (Jan) │ New (May) │ Old (Jan) │ New (May) │ │ 3.3% │ 3.1% ▼ │ 3.8% │ 4.4% ▲ │ └──────────────┴───────────────┴──────────────┴───────────────┘

The global economic backdrop against which India must operate has deteriorated noticeably over the first five months of 2026. The RBI noted that geopolitical risk has re-emerged as the dominant drag on global growth. The catalyst for this sudden deceleration was the late-February outbreak of hostilities in West Asia, an event that rapidly reverberated through global supply networks and commodity trading desks.

The IMF Baseline Revisions

Data from the International Monetary Fund (IMF) cited within the RBI report clearly illustrates the immediate cost of this geopolitical friction:

Global GDP Growth: The baseline forecast for worldwide economic expansion in 2026 has been revised downward to 3.1%, dropping from the 3.3% projection issued just months earlier in January.

Global Trade Volumes: The total volume of global merchandise and services trade is experiencing a sharp deceleration, now expected to crawl forward at just 2.8% for the year.

Global Inflation Surges: Conversely, worldwide cost-of-living metrics are climbing. The baseline projection for global inflation has been bumped up significantly to 4.4%, a stark increase from the previous January estimate of 3.8%.

Systemic Downside Risks to Global Trade

The central bank explicitly stated that any further intensification, lengthening, or widening of the West Asian geographical theater represents a profound systemic threat. The immediate consequences of the current conflict are already visible along primary maritime trade corridors:

Shipping Route Disruptions: Forcing logistics companies to divert vessels away from shorter, traditional passages has significantly inflated transit times.

Escalating Logistics Costs: Marine insurance premiums have skyrocketed, and container freight rates are tracking upward, creating an immediate “imported” inflationary impact for nations heavily reliant on global trade pipelines.

Equity & Tech Market Vulnerability: Beyond physical trade, the report warns that tighter macroeconomic conditions and a spreading “risk-off” sentiment could trigger massive capital reallocations. Specifically, the RBI highlighted that elevated valuations in technology sectors globally are due for a strict reassessment, raising the distinct probability of sharp corrections in international equity markets.

2. Fragmented and Resilient: The Key Pillars of India’s Macroeconomy

Despite this dark global horizon, the RBI maintains that the Indian economy is set to remain resilient in FY27. This defensive posture is not accidental; rather, it is the direct outcome of structural shifts that have minimized India’s vulnerability to external trade imbalances while maximizing internal production capacities.

┌─────────────────────────────────┐

│ INDIA'S FY27 RESILIENCE HUB │

└────────────────┬────────────────┘

│

┌─────────────────────────┼─────────────────────────┐

▼ ▼ ▼

┌─────────────────┐ ┌─────────────────┐ ┌─────────────────┐

│ Robust Domestic │ │ Lower Export │ │ Stable Policy │

│ Demand Engines │ │ Dependency Ratio│ │ & Capex Flow │

└─────────────────┘ └─────────────────┘ └─────────────────┘

Insulated via Low Export Dependency

One of India’s most significant contemporary advantages is its unique growth model. Unlike several East Asian or European manufacturing hubs, India features a relatively lower dependence on exports as its primary growth engine. While an international trade freeze still hurts, the vast majority of India’s GDP is generated, circulated, and sustained right within its borders.

The Corporate and Banking Balance Sheet Renaissance

The foundational strength of the domestic marketplace rests on the healthiest corporate and banking financial statements seen in over a decade:

Banking Sector Health: Thanks to years of aggressive regulatory reforms, prudent provisioning, and a dramatic cleanup of non-performing assets (NPAs), Indian commercial banks boast exceptionally thick capital buffers and highly stable credit growth patterns.

Corporate Deleveraging: India Inc. has spent the post-pandemic era aggressively deleveraging, paying down bad debt, and optimizing operational costs. This corporate financial health ensures that businesses possess the internal capacity to absorb rising input prices without immediately freezing capital expansions or cutting employment.

Sustained Public Capital Expenditure

The third pillar supporting this resilient trajectory is the Union Government’s unyielding commitment to infrastructure creation. The central bank highlighted that the government’s continued thrust on capital expenditure (capex) acts as a massive multiplier for economic activity. By funding large-scale national expressways, digital public infrastructure, and manufacturing corridors, public money is actively crowding in private investment, creating local jobs, and building long-term logistics efficiency that insulates the nation against external cost spikes.

3. Real GDP and Inflation Outlook for FY27

Balancing these internal structural strengths against severe external headwinds, the Reserve Bank of India has provided specific, calculated economic targets for the ongoing financial year.

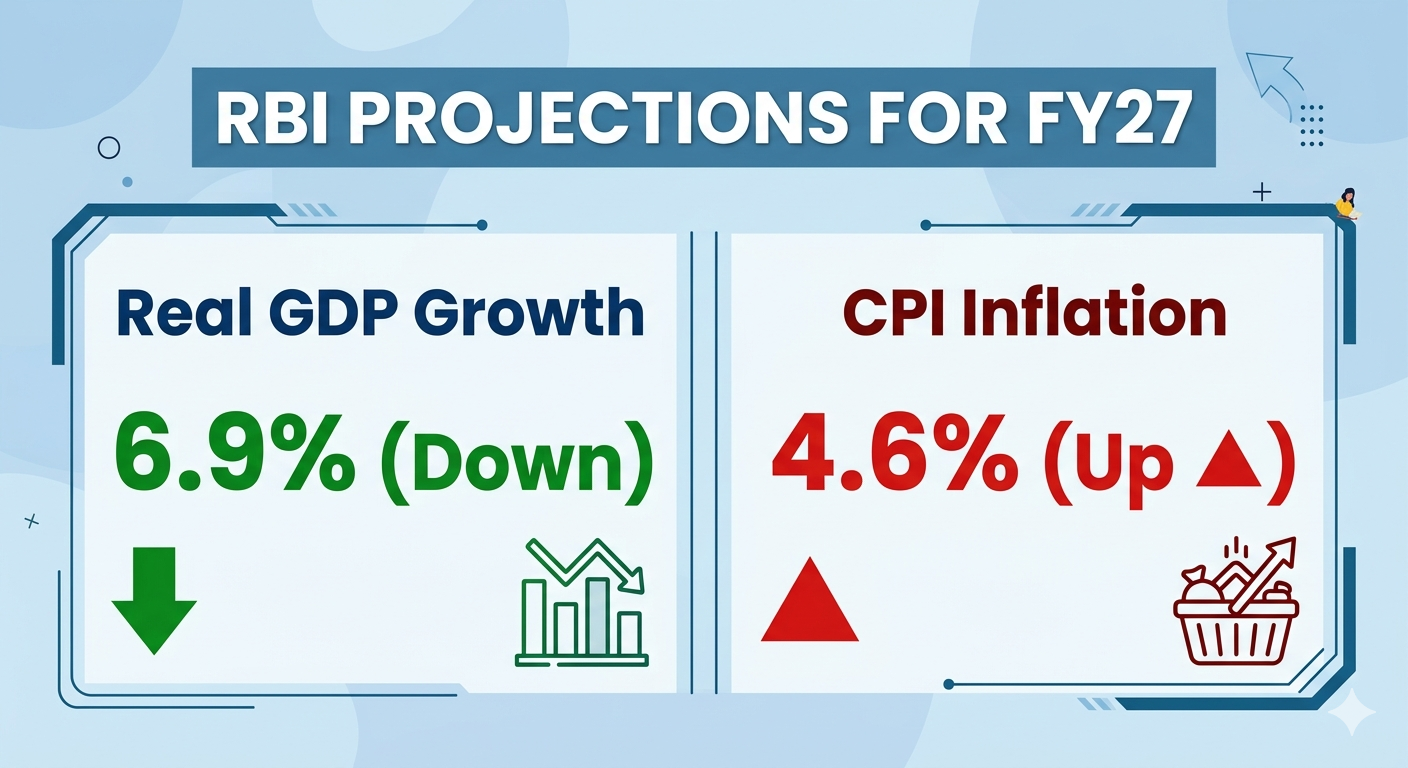

Real GDP Growth Projected at 6.9%

Assuming that the immediate military flashpoints in West Asia remain broadly contained and do not cascade into a wider regional war, the RBI projects real GDP growth for 2026-27 at 6.9%.

While this still positions India at the absolute top tier of major global growth performers, the central bank was careful to state that the risks remain tilted to the downside. If global energy prices sustain an extended upward run, or if domestic consumer sentiment takes a hit from sudden agricultural shocks, growth could face pressure toward the lower end of the band.

CPI Inflation Targeted at 4.6%On the price stability front, the central bank has forecast a headline Consumer Price Index (CPI) inflation rate of 4.6% for FY27. The RBI notes that while inflation is broadly on a path toward aligning with its medium-term targets, the trajectory is subject to considerable volatility, with risks strictly tilted to the upside.

The forces pushing against the RBI’s efforts to cool down prices include:

Global Commodity Volatility: Unpredictable spikes in crude oil and imported chemical intermediates due to the Middle Eastern shipping blockades.

Input and Wage Cost Spillovers: Rising manufacturing raw material costs slowly bleeding into corporate service sectors and urban wage structures.

Exchange Rate Fluctuations: Global currency market swings as international investors seek safe-haven assets like the US dollar, causing minor import-cost inflation through currency depreciation.

4. The Agricultural Equation: El Niño Threats and the Monsoon Wildcard

While international geopolitics dominate the headlines, the ultimate trajectory of India’s domestic inflation and rural consumption remains deeply tied to the skies. The RBI’s annual report dedicated substantial space to analyzing a critical domestic vulnerability: the health of the agricultural sector.

┌─────────────────────────────────────────────┐

│ SUMMER MONSOON DYNAMICS │

└──────────────────────┬──────────────────────┘

│

┌──────────────────────────┴──────────────────────────┐

▼ ▼

┌─────────────────────────────────┐ ┌─────────────────────────────────┐

│ EL NIÑO CONDITIONS (RISK) │ │ POSITIVE IOD (MITIGATION) │

├─────────────────────────────────┤ ├─────────────────────────────────┤

│ • Pacific ocean warming │ │ • Indian ocean warming pattern │

│ • Historically drives drought │ │ • Emerges in late summer │

│ • IMD projects 90% LPA rains │ │ • Acts as rain-inducing offset │

└─────────────────────────────────┘ └─────────────────────────────────┘

The IMD Below-Normal Monsoon Shock

Coinciding perfectly with the release of the RBI report, the India Meteorological Department (IMD) dropped a concerning update for the farming community. The IMD has officially forecast a below-normal monsoon season for 2026, with total cumulative rainfall over the crucial June-to-September window projected to settle at just 90% of the Long Period Average (LPA).

The Mechanics of El Niño vs. The Indian Ocean Dipole

The primary cause behind this weak monsoon forecast is the re-emergence of an El Niño event—the atypical warming of surface waters across the eastern Pacific Ocean. El Niño patterns are historically notorious for disrupting South Asian weather systems, frequently resulting in patchy rainfall, prolonged dry spells, low reservoir replenishment, and lower rural crop yields.

However, the RBI emphasized that all hope is not lost for the upcoming crop cycle. The country’s agricultural output is caught in a tug-of-war between two distinct marine phenomena:

The Downside (El Niño): Expected to impact early crop sowing, create above-normal summer temperatures, and lower baseline agricultural output across several critical food-producing states.

The Mitigation (Positive IOD): On a brighter note, meteorologists expect a positive Indian Ocean Dipole (IOD) pattern to develop toward the latter half of the monsoon season. A positive IOD refers to an ocean temperature differential that acts as a powerful rain-inducing mechanism for the Indian subcontinent. The RBI believes this late-season surge could effectively counteract or partially offset the early damage inflicted by Pacific Ocean warming.

Buffer Stocks as an Anti-Inflation Shield

Even if the monsoon distribution remains uneven, the central bank reassured markets that India’s structural food security remains intact. The country enters this challenging summer with highly adequate public foodgrain stocks and healthy baseline water levels across major national reservoirs. This strategic grain reserve ensures that the government possesses the tools necessary to counter speculative hoarders and manage sudden domestic market supply gaps.

5. Structural Reforms: Driving Labor and Trade Competitiveness

Rather than simply operating on the defensive, the RBI’s report outlines an active, forward-looking series of domestic structural transformations designed to unlock long-term productivity gains.

Full-Scale Implementation of the Four Labor Codes

A major catalyst for internal market optimization in FY27 will be the comprehensive, nationwide roll-out of India’s long-delayed four unified labor codes. The central bank predicts that this regulatory consolidation will fundamentally streamline manufacturing compliance, strengthen worker social security networks, and eliminate bureaucratic red tape. This environment is projected to noticeably improve domestic labor market conditions, driving up both structural productivity and employment numbers across formal sectors.

Trade Treaties and Altering the Export Mix

To fight the realities of a protectionist global market, India is completely reworking its international trade playbook:

| Strategic Trade Driver | Macroeconomic Objective | Expected Impact in FY27 |

| Bilateral Trade Agreements | Bypassing gridlocked multilateral frameworks to ink direct deals with key European, African, and Asian economies. | Boosts Foreign Portfolio Investment (FPI) and opens new export pathways. |

| Frontier Sector Scaling | Aggressive state support for local manufacturing in advanced fields like semiconductors, electronics, and green tech. | Enhances long-term export competitiveness and reduces critical import reliance. |

| Services Export Resilience | Leveraging global capability centers (GCCs) to scale specialized software, design, and high-end business services. | Continues to anchor the nation’s overall services trade balance. |

| Remittance Diversification | Shifting reliance away from volatile Gulf economies toward skilled labor corridors in non-Gulf nations. | Acts as a stable, predictable buffer for the current account balance. |

6. Financial Stability: A Resilient Banking Arena with Minor Headwinds

The health of a nation’s financial system determines how effectively it can withstand prolonged real-world stress. The RBI’s Annual Report confirms that the Indian financial architecture is in excellent shape, although asset managers must prepare for unique market pressures over the next twelve months.

Prudent Regulations and Adequate Buffers

The domestic financial framework enters FY27 backed by a series of proactive, counter-cyclical regulatory actions taken by the central bank over the previous two years. Indian lenders have maintained strong capital adequacy ratios and healthy internal profit reserves, providing them with more than enough buffer to withstand unexpected macro shocks.

Two Key Micro-Risks to Watch

Despite this broad health, the RBI advises banks to remain watchful on two specific fronts:

Corporate Earnings Compress: Continuous global supply chain friction and erratic input prices could compress profit margins for mid-sized corporate borrowers. If these stresses persist, they could cause minor, localized deteriorations in specific commercial loan portfolios.

Sovereign Yield Pressures: Because global central banks are keeping interest rates higher for longer to combat sticky international inflation, sovereign bond yields are expected to remain elevated. This environment could put pressure on the investment portfolios of domestic banks, requiring careful treasury management to minimize mark-to-market accounting losses.

On balance, however, the central bank’s verdict is clear: the Indian financial universe has built up sufficient institutional buffers to absorb these adverse shocks without disrupting the wider flow of credit to productive sectors of the economy.

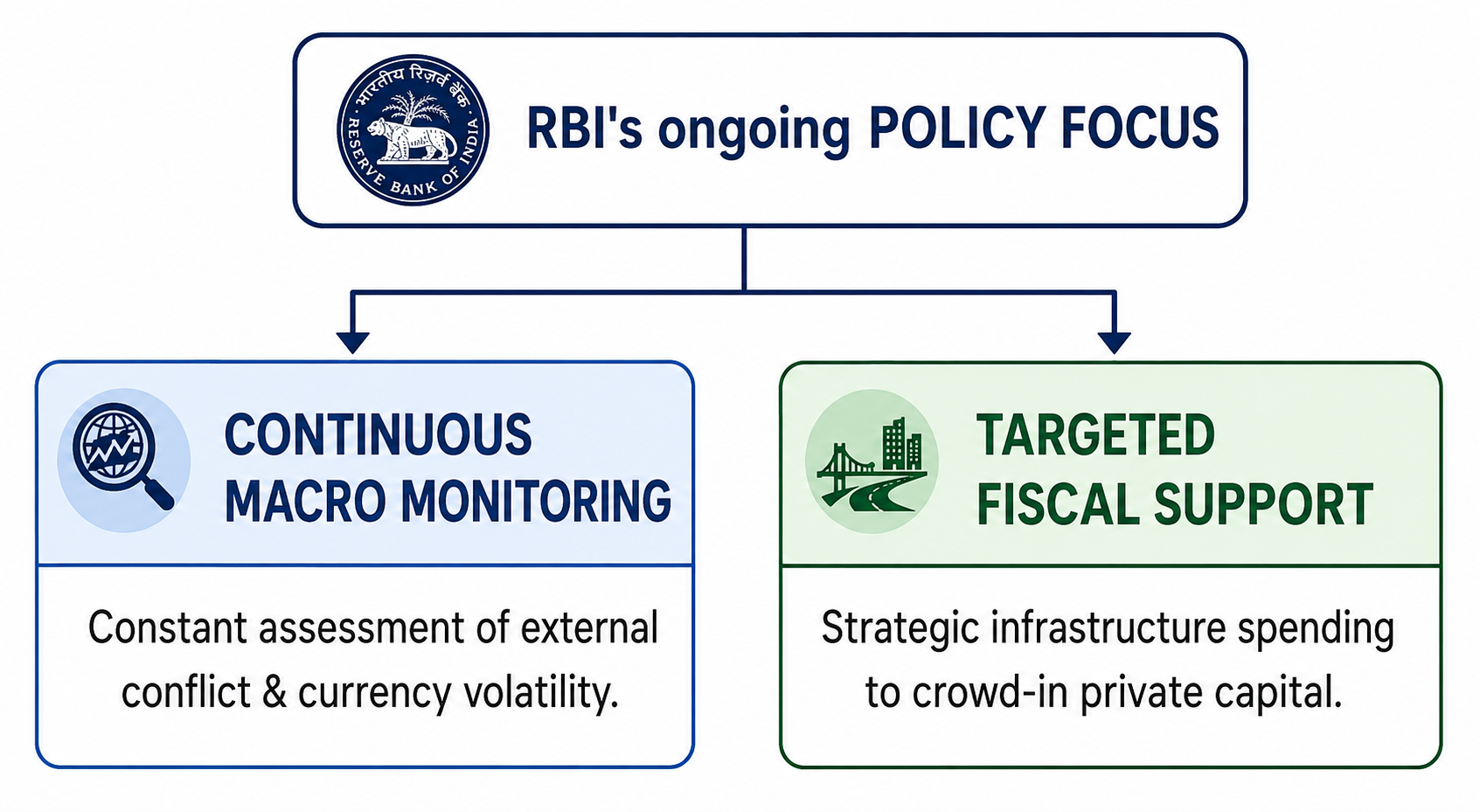

7. Strategic Outlook and Policy Conclusions

The Reserve Bank of India’s Annual Report for 2025-26 concludes with a strong reminder that while India’s internal economic momentum is undeniably powerful, complacency is a luxury the country cannot afford.

The combination of robust domestic demand, historic balance sheet cleanups, and a highly stable policy environment provides India with a distinct competitive edge in an otherwise highly unstable global economy. However, because the external environment remains incredibly volatile, policy makers must remain deeply agile.

The RBI has committed to a policy of continuous, real-time assessment of evolving macroeconomic factors. This approach means the central bank stands ready to deploy nimble monetary adjustments, liquidity management techniques, and targeted regulatory interventions on an ongoing basis. By pairing domestic economic development with a watchful eye on global risks, India is fundamentally equipped to turn a year of international crisis into an exhibition of enduring domestic strength.

Disclaimer:This information is based on various inputs from news agency