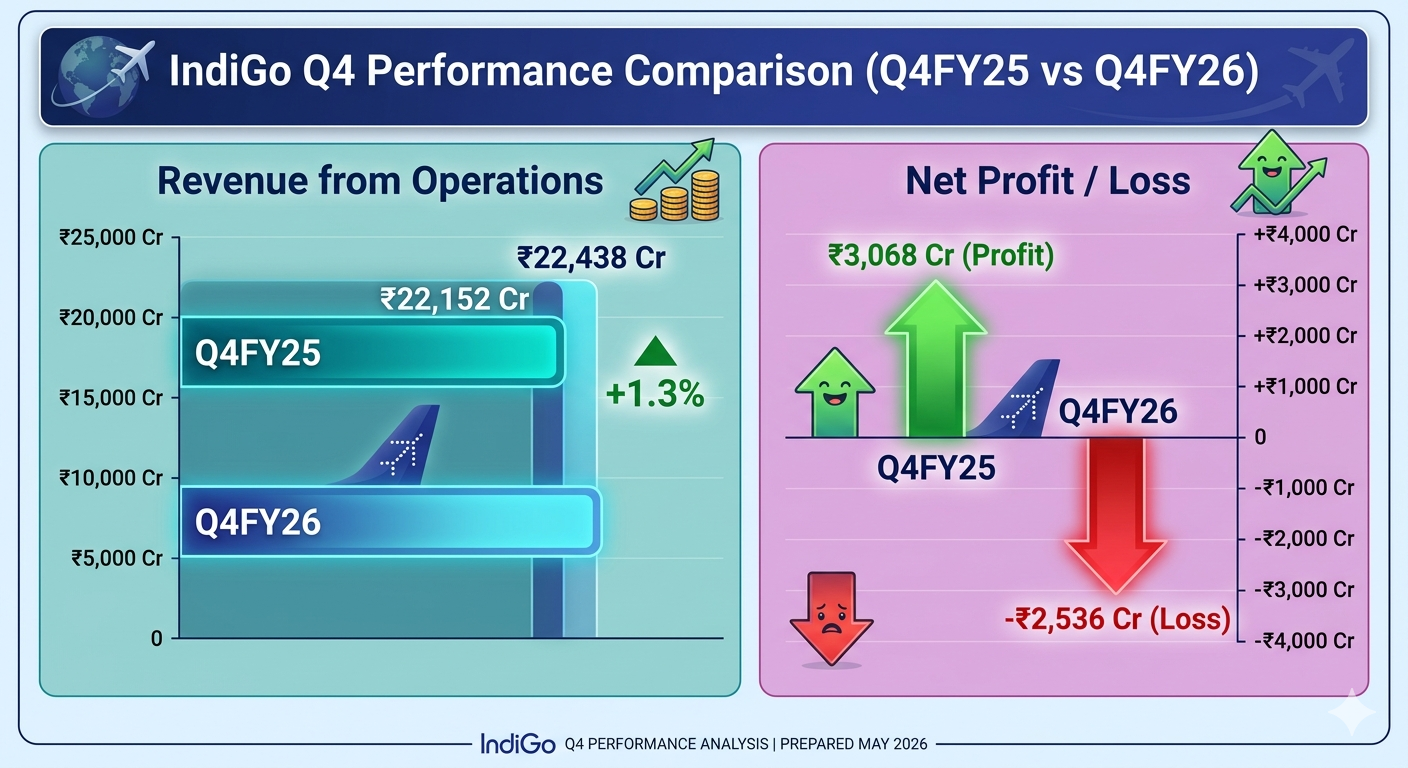

India’s biggest airline, IndiGo Q4 Results, reported a major financial shock on Friday. According to its latest quarterly results, the airline suffered a massive net loss of ₹2,536 crore for the final quarter ending March 31, 2026. This is a huge drop compared to the same time last year, when the airline made a solid profit of ₹3,068 crore.

Even though IndiGo managed to keep its planes full and expand its flights across India, it could not beat a series of tough economic challenges. The airline’s management stated that three main problems completely wiped out their profits:

A very sharp drop in the value of the Indian rupee

Big changes in labor laws that raised operational costs

A highly unstable global trading environment

Breaking Down the Financial Damage: Revenue vs. Net Profit

When you look closely at the operational metrics, the airline’s underlying business actually managed to hold its ground, which makes the ultimate net loss even more surprising. This creates a sharp contrast between incoming customer revenue and bottom-line profitability.

The airline’s revenue from operations actually grew marginally during the fourth quarter, creeping up by 1.3% to hit ₹22,438 crore, compared to the ₹22,152 crore it generated in the corresponding quarter of the previous fiscal year. However, this mild top-line growth was completely overwhelmed by exploding operating costs, currency fluctuations, and one-time exceptional financial hits.

During this specific three-month period, the carrier had to absorb a substantial one-time charge of ₹250 crore. When combined with skyrocketing aviation turbine fuel (ATF) bills and a steadily weakening local currency, these expenses created a major financial drain. This drain rapidly turned a healthy operating profit into a steep net loss, shocking everyday retail investors on Dalal Street.

The Macroeconomic Enemies: Rupee Depreciation, Fuel Prices, and Labor Laws

The corporate filing highlights three major systemic issues that disrupted the airline’s financial calculations. These factors were largely outside of management’s direct control, showcasing the vulnerabilities faced by modern aviation companies:

1. The Sudden Drop of the Indian Rupee

In commercial aviation, a massive chunk of an airline’s ongoing expenses is designated in US dollars. This includes aircraft lease rentals, overseas maintenance, repair, and overhaul (MRO) contracts, and international airport landing fees. As the Indian rupee suffered a sharp depreciation over the last few quarters, the cost of servicing these dollar-denominated liabilities shot up significantly. Even though the airline was collecting ticket fares in rupees, it had to pay its major structural bills in highly expensive dollars, creating a significant foreign exchange transaction loss.

2. Changing Dynamics in Labor Laws

The domestic aviation landscape has seen sweeping regulatory updates regarding pilot fatigue management, flight duty time limitations (FDTL), and revised crew compensation structures. Implementing these mandatory labor law changes required the airline to quickly hire, train, and deploy a larger pool of flight crew members to maintain its daily schedule. This regulatory shift caused a sharp, structural increase in employee benefit expenses and operational overheads during the fourth quarter.

3. High Aviation Turbine Fuel (ATF) Costs

Geopolitical instability across global energy corridors kept crude oil prices highly volatile throughout the winter. Because jet fuel makes up anywhere from 40% to 45% of a typical Indian budget carrier’s total operating cost, even a minor upward movement in local ATF prices cuts directly into profit margins. The airline found it difficult to pass these rapidly escalating fuel expenses onto consumers through higher ticket fares without hurting passenger demand.

Passenger Traffic and Fleet Efficiency Metrics

The underlying operational data shows that consumer demand for air travel remains robust across India, even if macro factors are squeezing corporate margins.

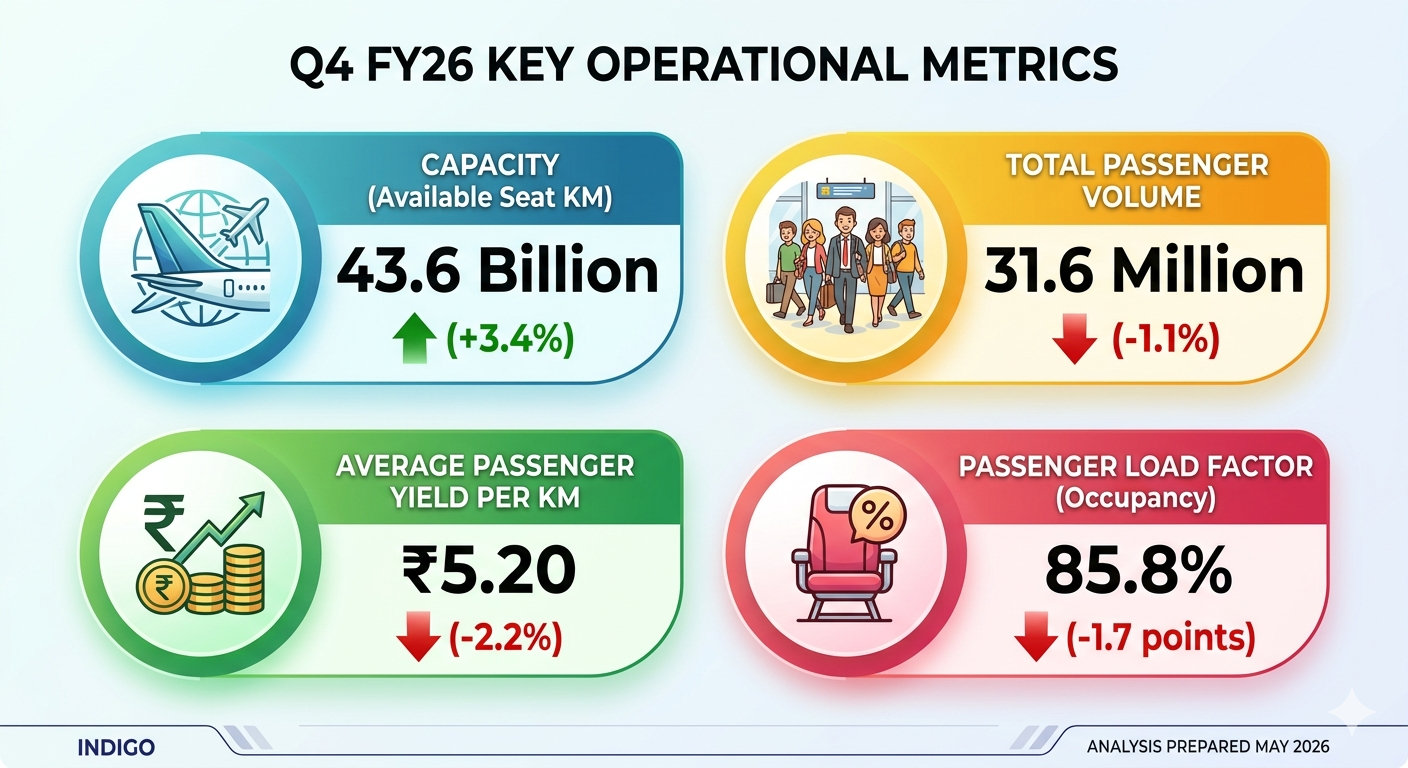

The low-cost carrier reported that its overall capacity grew by 3.4% during the quarter, reaching a total of 43.6 billion Available Seat Kilometers (ASKs). This capacity growth is particularly impressive considering the continuous operational challenges and airspace route diversions forced by ongoing geopolitical conflicts across the Middle East.

However, a closer look at efficiency reveals minor pressure on pricing power. Total passenger volumes dipped very slightly by 1.1%, down to 31.6 million travelers for the quarter. Simultaneously, the passenger yield—the average amount of money collected per passenger for every kilometer flown—softened by 2.2% to slide down to ₹5.20.

The airline’s average passenger load factor (seat occupancy) also experienced a minor decline, dropping by 1.7 percentage points to settle at 85.8%. This tells us that while the airline successfully added more seats to the sky, ticket pricing had to be adjusted slightly lower to keep those seats filled in a highly competitive domestic market.

Management Insights: Finding Core Strength Amid Market VolatilityDespite the heavy net loss reported in the IndiGo Q4 results, corporate leadership remains firmly optimistic about the long-term strategic direction of the enterprise. The executive team emphasized that if you look past the unpredictable foreign exchange fluctuations and one-time accounting hits, the core engine of the business is performing well.

“Fiscal year 2026 was marked by an exceptionally challenging operating environment, which materially impacted our final profitability. Despite these tough external conditions, the underlying performance of our core business remained highly resilient. During the full year, our overall capacity grew by 9.5% and our total income increased by over 6%.” — Rahul Bhatia, Managing Director of InterGlobe Aviation.

Bhatia went out of his way to offer deeper analytical context for institutional shareholders, revealing a hidden silver lining in the full-year performance. He explained that if you completely strip away the negative impacts of foreign exchange fluctuations and exceptional non-recurring items, the airline actually delivered a robust full-year profit of ₹7,500 crore.

The company continues to maintain a rock-solid balance sheet backed by substantial cash liquidity, proving its structural ability to navigate long periods of intense market volatility without disrupting its massive long-term aircraft purchase commitments.

Strategic Shift: Capital Allocation and Fleet Ownership Plans

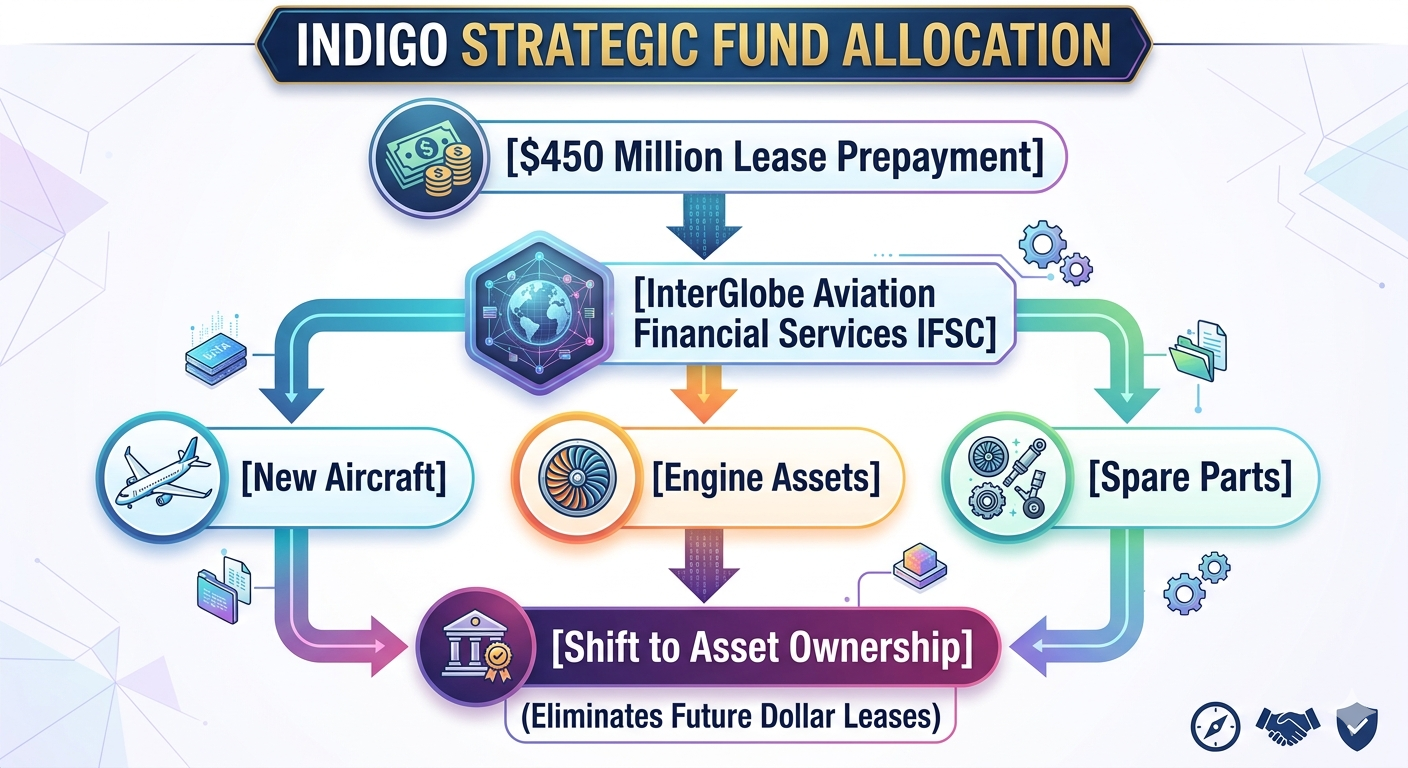

In a major corporate governance move announced alongside the earnings release, the board of directors approved a massive capital reallocation strategy. The board greenlit the partial prepayment of the company’s existing finance lease obligations to its wholly-owned subsidiary, InterGlobe Aviation Financial Services IFSC Private Limited.

This financial restructuring will move in one or more structured tranches, involving a massive aggregate amount of up to $450 million (approximately ₹3,750 crore).

These designated corporate funds will be systematically used by the IFSC subsidiary to directly acquire high-value aviation assets. This approach will allow the parent company to secure direct ownership of its aircraft, jet engines, and critical spare parts, rather than relying strictly on expensive external lease rentals.

Over the long term, moving from a pure lease-and-rent model to an asset-ownership model should drastically lower the airline’s fixed dollar-denominated expenses. This shift will insulate its future quarterly earnings from the wild swings of the global foreign exchange market.

Dalal Street Reactions: Stock Value Slides Ahead of the AnnouncementTraders and institutional funds on Dalal Street clearly anticipated a tough quarter, leading to a visible sell-off ahead of the official data release. On Friday, shares of InterGlobe Aviation opened weak and faced steady selling pressure throughout the day, eventually closing 3% lower at ₹4,420 apiece on the Bombay Stock Exchange (BSE).

Because the official stock exchange announcement landed during post-market hours, the full impact of this ₹2,536-crore net loss will only be visible when the opening bell rings on Monday morning. Market analysts expect the stock to face short-term pressure as algorithmic trading desks adjust their near-term price targets to reflect the drop in profitability.

However, long-term portfolio managers will likely pay close attention to the airline’s healthy cash reserves and its ambitious $450-million lease prepayment strategy. These factors demonstrate strong financial health despite the ugly net headline numbers.

Sector-Wide Outlook: What This Means for Indian AviationThe disappointing corporate numbers serve as a stark warning for the broader Indian aviation landscape. If the country’s most operationally efficient, cost-conscious, and well-capitalized airline is swinging heavily into the red due to macro pressures, smaller regional carriers are likely facing even tougher conditions.

The domestic aviation industry continues to deal with a severe structural imbalance. While passenger demand is hitting historic highs as millions of middle-class Indians choose to fly, the cost of running an airline in India remains incredibly high. High state taxes on jet fuel, expensive airport infrastructure charges, and an unavoidable exposure to global dollar fluctuations make it very difficult to achieve steady profitability.

As the industry moves into the seasonally weaker monsoon quarter, airlines will have to carefully manage their seat capacity, avoid aggressive price wars, and focus heavily on cost optimization to protect their cash flows.

Technical Analysis and Near-Term Stock Levels

For active derivatives traders and equity investors, the technical setup on the daily charts for InterGlobe Aviation indicates a shift in near-term momentum. The stock has been trading in a steady ascending channel for several months, but Friday’s 3% slide has pushed the price action right down to its crucial 50-day Exponential Moving Average (EMA) located near the ₹4,400 mark.

If the stock breaks below the ₹4,400 support level on Monday morning due to a knee-jerk reaction to the net loss, the next major historical demand zone sits around ₹4,250, where the 100-day EMA should provide strong support.

Conversely, if the market focuses on the underlying core profit of ₹7,500 crore (excluding forex adjustments) and the proactive $450-million debt reduction move, the stock could quickly form a bottom near current levels. It may then attempt to climb back up to retest its overhead resistance barriers situated at ₹4,650 and ₹4,780.

Navigating the Competitive Landscape and Long-Term Strategy

Looking past the immediate financial shock of the quarter, the long-term growth story of Indian aviation remains tied to network expansion and market consolidation. The low-cost carrier still commands a dominant market share of over 60% in the domestic skies, giving it massive pricing power and unmatched economies of scale. This scale allows it to secure deep volume discounts from global aerospace manufacturers like Airbus and Pratt & Whitney, something smaller domestic rivals simply cannot replicate.

IndiGo Strategic Path Forward:

Short-Term Challenge ──► Manage Fuel Volatility & Crew Overhead Costs

Medium-Term Action ──► Deploy $450 Million to Buy Fleet Assets Directly

Long-Term Goal ──► Expand High-Yield International Routes

The key to unlocking steady, predictable profitability over the next decade lies in expanding high-yield international routes. By flying to more destinations across Europe, Central Asia, and the Middle East, the airline can collect a larger share of its ticketing revenue directly in foreign currencies.

This structural shift will create a natural hedge against the depreciation of the Indian rupee, ensuring that its incoming cash flows match its dollar-denominated aircraft lease and maintenance liabilities. Combined with the strategic move to buy aircraft directly through its IFSC subsidiary, this international push will help the airline break free from the macro cycles that disrupted its financial performance this quarter.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investors are advised to do their own research or consult with a certified financial advisor before making any investment decisions on the stock market.