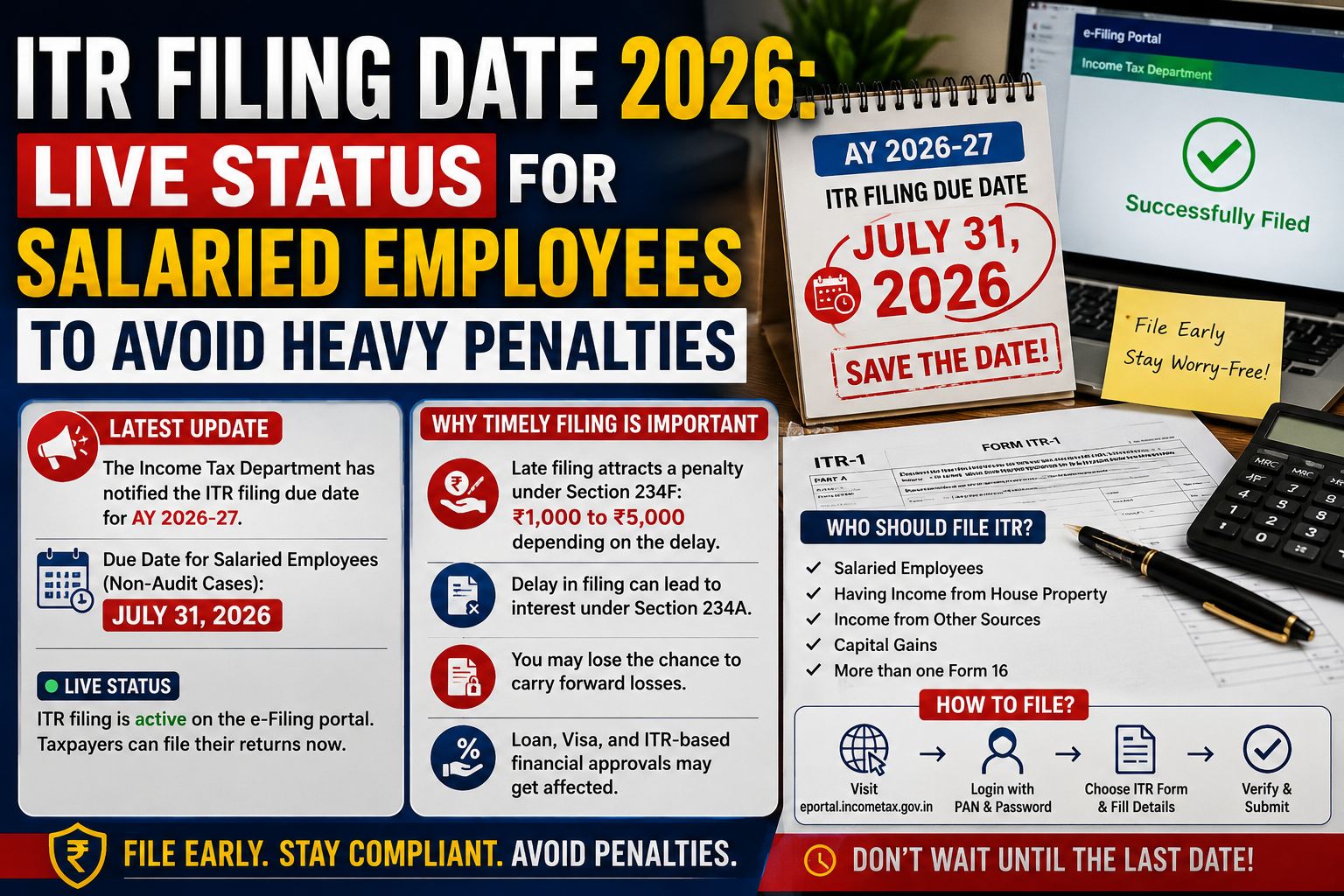

The official ITR Filing Date 2026 season has unexpectedly kicked off ahead of its usual timeline. The Income Tax Department has officially rolled out both the offline Excel utility and the direct online filing modules for specified tax return forms. For millions of salaried professionals across India, this structural rollout officially marks the commencement of the income tax return filing phase for Assessment Year 2026-27 (corresponding to Financial Year 2025-26).

While the administrative gateway is open, making immediate electronic submission functional, individual taxpayers must navigate specific structural prerequisites—most notably the issuance of organizational wage statements and the synchronization of global internal asset accounts—before clicking the final submission link.

Current Activation Status of E-Filing Gateways

The Central Board of Direct Taxes (CBDT) has enabled structural functionalities progressively across its digital frameworks. Eligible individuals can execute their submissions directly on the web-based utility or utilize the downloadable spreadsheets to construct an offline dataset, subsequently generating the mandatory compiled data schema file for portal transmission.

+-------------------------------------------------------------------------+

| AY 2026-27 E-FILING PORTAL MATRIX |

+----------------------+--------------------+-----------------------------+

| Tax Return Form | Gateway Status | Mode of Compilation |

+----------------------+--------------------+-----------------------------+

| ITR-1 (Sahaj) | LIVE & ACTIVE | Online Portal / Excel Tool |

| ITR-2 | DEACTIVATED / PEND | Awaiting Department Release |

| ITR-4 (Sugam) | LIVE & ACTIVE | Online Portal / Excel Tool |

+----------------------+--------------------+-----------------------------+

As illustrated, the department has prioritized forms handling structurally simplified income streams. Taxpayers whose financial profile mandates the deployment of complex schedules remain structurally paused until secondary structural releases are deployed by the e-filing technical division.

Analysis of Form Eligibility Parameters for ITR Filing Date 2026 -27

Selecting an inappropriate filing form results in an automatic “Defective Return” notice under Section 139(9) of the Income Tax Act, rendering the entire filing void. The operational boundaries for the currently active and pending forms are strictly defined.

1. The Scope of ITR-1 (Sahaj)

This streamlined single-page form is exclusively reserved for resident individual taxpayers whose aggregate domestic earnings for the fiscal duration do not cross the absolute structural boundary of ₹50 Lakh. The source parameters must conform strictly to the following categories:

Direct monthly compensation or corporate pension distributions.

Single domestic housing property ownership (where interest or rental calculations do not involve complex multi-property carry-forward deficits).

Secondary miscellaneous capital receipts, encompassing basic domestic bank account interest, fixed deposit yields, family pension adjustments, and corporate dividend credits.

Restricted agrarian receipts up to a maximum structural threshold of ₹5,000.

2. The Complex Mechanics of ITR-2

For salaried employees who find themselves excluded from the basic parameters of Form 1, ITR-2 serves as the primary alternate legal vehicle. This structure applies to individuals and Hindu Undivided Families (HUFs) who do not possess any organizational profits or business revenues, yet exhibit complex financial traits:

Aggregate annual financial inflows outstripping the ₹50 Lakh threshold.

Domestic or international investment portfolio changes generating short-term or long-term capital gains or losses.

Ownership stakes distributed across multiple domestic real estate properties.

Unlisted equity shareholdings or registered corporate directorships held at any point during the financial period.

Assets or financial interest located outside India, which requires mandatory reporting in Schedule FA.

The Form 16 Mismatch Trap: Why Early Action Demands Caution

Critical Filing Precaution

Even though the e-filing portal is operational, you should not finalize your tax return until your employer officially issues your Form 16 and the Income Tax Department fully refreshes your Annual Information Statement (AIS).

[Employer Processing] ---> Generates Form 16 (Deadline: June 15)

|

[Portal Syncing] ---> Updates AIS & Form 26AS Portals

|

[Taxpayer Execution] ---> Cross-Checks Mismatches & Files ITR

Corporate entities are legally permitted until June 15 to process and upload consolidated Tax Deducted at Source (TDS) statements for the fourth quarter. Consequently, filing a return using provisional personal ledger records prior to these systematic reconciliations risks structural contradiction with central accounting records.

If your submitted numbers deviate from the tax credits captured inside the system’s live databases, internal processing routines flag the account automatically. This triggers computational mismatch notifications or delays the disbursement of legitimate tax refunds.

Statutory Timelines and Penal Deficit Computations

For individual accounts not subject to mandatory commercial regulatory audit, the terminal statutory date to conclude standard return processing is fixed at July 31, 2026. Failing to meet this legal milestone triggers a sequential chain of financial penalties under current tax laws.

+--------------------------------------------------------------------------+

| PENAL STRUCTURE FOR POST-DUE DATE FILINGS |

+------------------------+-----------------------+-------------------------+

| Total Taxable Income | Delay Filing Period | Legal Fee (Sec 234F) |

+------------------------+-----------------------+-------------------------+

| Gross Income ≤ ₹5 Lakh | Aug 1 – Dec 31, 2026 | ₹1,000 |

| Gross Income > ₹5 Lakh | Aug 1 – Dec 31, 2026 | ₹5,000 |

| Any Taxable Tier | Post Dec 31, 2026 | Barred (Unless ITR-U) |

+------------------------+-----------------------+-------------------------+

Accumulative Interest Liabilities (Section 234A)

Apart from the upfront late filing fees, missing the July deadline triggers interest charges on any unpaid tax liability under Section 234A. The system levies an accumulative monthly interest rate of 1% (or part of a month) on the outstanding net tax payable. This balance is calculated starting from August 1 and continues mounting until the taxpayer completes verification.

The Forfeiture of Capital Loss Offsets

A major hidden financial consequence of late submission is the immediate loss of investment asset relief. If you file your tax return after the July 31 deadline, you lose the legal right to carry forward any short-term or long-term capital losses incurred during the year. These losses cannot be used to offset future profitable asset sales, which can increase your long-term tax burden.

A Step-by-Step Guide to Secure Digital E-Filing

To execute a clean, unassisted submission directly through the central tax platform, complete the following steps in sequence:

Accessing the Portal: Open your browser and navigate to the official portal link at

(https://www.incometax.gov.in/). Log in using your secure credentials, which use your Permanent Account Number (PAN) or your verified Aadhaar identifier as the primary login ID.Data Verification: Navigate to the ‘e-File’ drop-down options, select the ‘Income Tax Returns’ path, and launch the Annual Information Statement (AIS) alongside your Form 26AS. Confirm that every entry for corporate salary payouts, withholding tax deductions, and high-value bank interest credits exactly matches your personal financial records.

Form and Regime Selection: Select the ‘File Income Tax Return’ button, choose the correct Assessment Year, and select the filing method. The system will prompt you to choose between the default New Tax Regime (with its restructured slab system) and the alternate Old Tax Regime.

Validating Pre-Filled Information: Review the pre-populated structural segments. The portal automatically maps verified historical details into your personal profile, tax credit fields, and bank account registers. Update any new fields, including mandatory sections for institutional loan schedules or specific asset declarations.

Final Submission and Authentication: Verify the final tax computation matrix, settle any remaining self-assessment liabilities through net banking, and submit your return data. You must complete electronic verification within the statutory 30-day window, using an Aadhaar-linked mobile OTP or an authorized bank account validation code, to officially close your case file.

Summary of Key Parameters

Operational Status: Active online/offline data tools for Form 1 and Form 4; Form 2 remains offline.

Filing Window Deadline: Initial general filing phase ends on July 31, 2026.

Late Fee Penalty: Up to ₹5,000 under Section 234F, combined with 1% monthly interest charges under Section 234A.

Core Prerequisite: Wait for your employer to upload the Q4 data and issue your Form 16 before submitting.

FAQ: Essential Answers for This Filing Cycle

Q1: Can I submit my return if the e-filing system shows my Form 26AS is blank?

No. A blank or partially updated Form 26AS indicates that your employer or banking institution has not yet uploaded their formal quarterly tax withholding reports. If you submit your return before these entities update the central database, the system’s processing routines will flag your file for mismatched tax credits.

Q2: I am a salaried individual with an active intraday stock trading portfolio. Can I use ITR-1?

No. Speculative stock transactions and short-term capital changes require advanced reporting forms. You must wait for the release of ITR-2 or utilize ITR-3 if your equity trades are categorized as formal business or professional activities.

Q3: What happens if I fail to complete the electronic verification step after submitting my return?

Your submission remains incomplete until verified. If you do not authorize the data within 30 days of uploading, the system treats the entire transaction as “Incomplete/Never Filed.” This can lead to late fees and processing delays, just like missing the original deadline.