RVNL Q4 results are officially out, sending waves through the Indian stock market and leaving retail investors with a massive basket of questions. Rail Vikas Nigam Limited (RVNL), the public sector undertaking under the Ministry of Railways, recently submitted its financial scorecard for the final quarter of the fiscal year 2026 (Q4 FY26) to the stock exchanges. The headline numbers present a striking paradox: while the infrastructure giant managed to push its topline revenue marginally upward, its bottom-line net profits witnessed a staggering, near-60% nosedive.

For an organization that has been one of the darlings of the public sector enterprise (PSU) stock rally over the last couple of years, this sharp deceleration in profitability serves as a stark reality check. In this comprehensive, deep-dive analysis, we break down the core operational metrics, explore why the company’s margins shrank so drastically, evaluate the latest dividend announcement, and analyze what these developments mean for long-term shareholders moving forward.

RVNL Q4 results Core Financial Blueprint: Revenue vs. Net Profit

To understand the health of any corporate entity, one must look at the push-and-pull relationship between income and actual earnings. The Consolidated Year-on-Year (YoY) metrics for RVNL’s fourth quarter tell a highly dramatic story of escalating costs swallowing up revenue gains.

Topline Stability with Marginally Improving Revenue

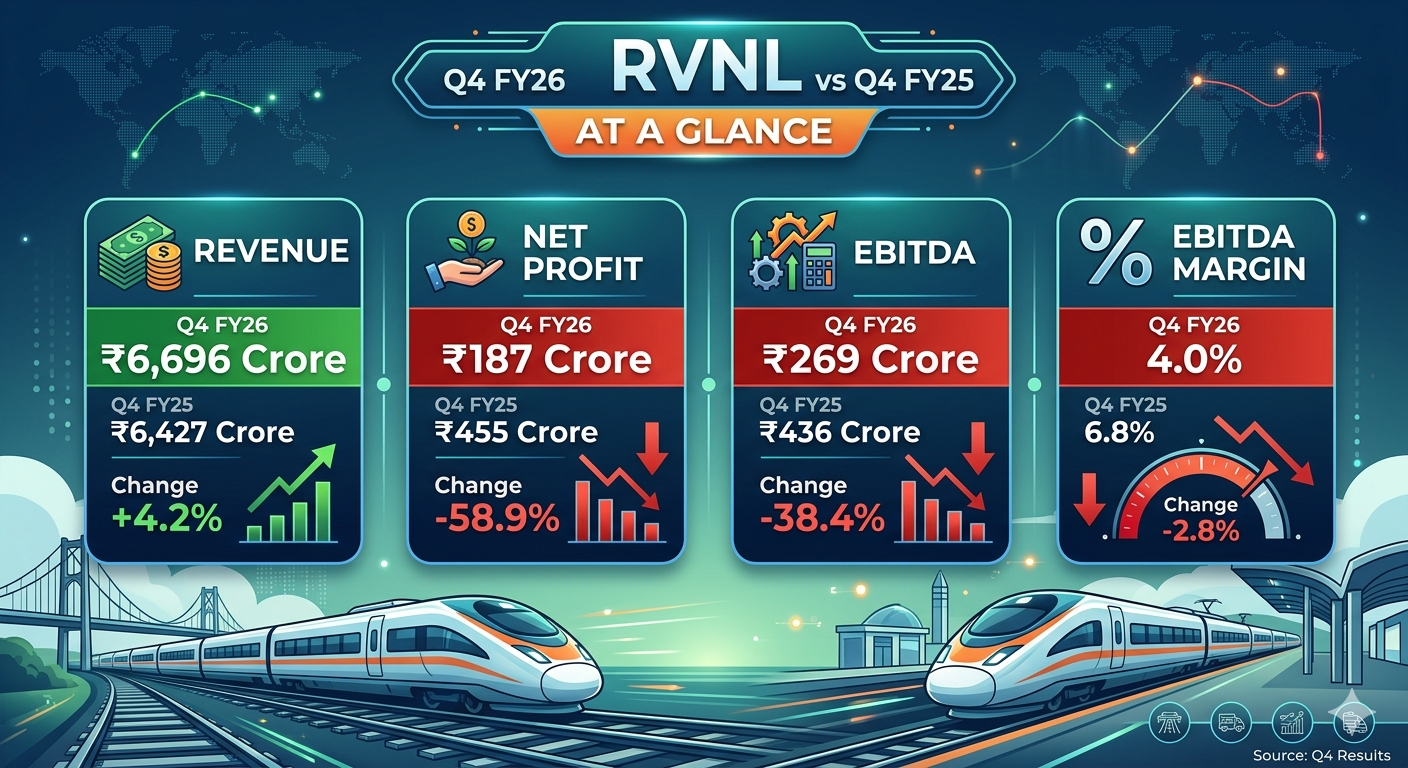

During the quarter ended March 31, 2026, RVNL reported a consolidated revenue from operations of ₹6,696 crore. When weighed against the ₹6,427 crore revenue pulled in during the corresponding fourth quarter of the previous fiscal year (Q4 FY25), this represents a year-on-year growth of 4.2%.

While a 4.2% increase is modest—especially for an infrastructure company sitting on a massive, multibillion-dollar order book—it demonstrates that project execution and billing lines have remained functional. The company is actively working on its domestic rail, metro, and cross-border infrastructure commitments, ensuring that cash inflow channels remain open.

The Bottom-Line Collapse

The true shockwave of the earnings report lies in the net profit metrics. Rail Vikas Nigam Ltd saw its consolidated net profit plummet by 58.9%, landing at ₹187 crore for Q4 FY26. To put this into perspective, the railway PSU had registered a robust net profit of ₹455 crore during the same exact period in fiscal year 2025.

Losing more than half of your net profit in a year-on-year comparison is an alarming signal for equity analysts. It highlights a fundamental breakdown between making sales and retaining cash. Essentially, while RVNL succeeded in executing more work on the ground, the financial return for doing that work shrank to a fraction of its former self.

Dissecting the Margin Squeeze: The EBITDA Story

To understand why a company’s profits can crash while its revenue grows, we have to look directly at the operating performance, specifically measured through EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) and operating margins.

The Weakened Operating Engine

RVNL’s operating performance during the March quarter took a severe beating. The company’s EBITDA fell by 38.4%, dropping down to ₹269 crore against ₹436 crore in the previous fiscal year’s matching quarter.

When EBITDA falls significantly faster than revenue rises, it indicates that the fundamental cost of doing business has escalated. For an infrastructure developer, these costs usually boil down to:

Escalating raw material prices (steel, cement, specialized components).

Higher sub-contracting and labor expenses.

Logistical bottlenecks that prolong project timelines, resulting in costly overhead extensions.

Lower-margin projects constituting a larger portion of the current revenue mix.

The Shrinking Profit Margin Range

As a direct outcome of the operating cost spike, RVNL’s EBITDA margin contracted severely to 4%, down from 6.8% in the prior-year quarter.

In the high-volume, capital-intensive infrastructure space, a margin cushion of 6.8% is already relatively lean. Dropping down to a razor-thin 4% leaves the company virtually zero room for operational errors, regulatory delays, or material waste. This contraction is the primary culprit behind the ₹187 crore net profit figure.

The Dividend Dynamics: Lowest Final Payout in Three YearsAmidst the disappointing earnings figures, the board of directors at RVNL attempted to offer some structural reassurance to its loyal shareholder base by declaring a final dividend. However, even this silver lining carries the weight of the company’s financial tightening.

Breaking Down the Dividend Distribution

Despite the steep slump in net earnings, RVNL announced a final dividend of ₹0.71 per equity share for the fiscal year 2026. This corporate action translates into an aggregate payout of approximately ₹148.03 crore distributed directly to the company’s equity shareholders.

Important Operational Note: The record date to ascertain which shareholders are entitled to receive this final dividend has not yet been locked in by the management. According to the regulatory exchange filings, this payout is strictly subject to formal approval by company members at the upcoming Annual General Meeting (AGM). Once approved at the AGM, the final dividend will be credited to eligible bank accounts within 30 days.

Tracking the Full-Year Dividend Horizon

To evaluate the true value of the stock’s yield, we have to look at the combined dividend payouts across the entirety of fiscal 2026:

February 2026: RVNL issued a robust interim dividend of ₹1.00 per share.

May 2026 (Current Declaration): The company added a final dividend of ₹0.71 per share.

Total Fiscal 2026 Dividend: This brings the cumulative yearly payout to ₹1.71 per share.

While the ₹0.71 final dividend marks the lowest standalone final dividend declared by the firm since 2023, the total combined payout for the year (₹1.71) is only marginally lower than what was seen in fiscal 2025, thanks to the heavier weight of the February interim payment.

Historical Comparison Context

For long-term tracking, it helps to glance backward at how the company has rewarded investors via dividends over recent cycles:

Fiscal 2025 Payout Highlights: Hindalco on August 21, 2025, delivered a dividend of ₹1.72 per share, presenting an interesting cross-sector yield comparison, whereas RVNL’s previous full cycles hovered near similar benchmarks.

September 2024: The company delivered a dividend payout of ₹2.11 per share.

September 2023: RVNL rewarded its investors with a dividend payout of ₹0.36 per share.

Market Implications: How Investors Should Navigate the News

The stock market is an inherently forward-looking mechanism. Often, when an asset’s price runs up on high expectations, a sudden drop in core operating performance can trigger sharp corrections.

Valuation Realities vs. Growth Expectations

For the past several quarters, railway PSUs have traded at historically high Price-to-Earnings (P/E) multiples, driven by the Indian Government’s massive capital expenditure allocation toward national rail modernization, Vande Bharat expansions, and dedicated freight corridors.

However, a 4% EBITDA margin raises fundamental questions about structural valuation. If RVNL must spend significantly more to execute its order book, its high P/E multiple will face downward pressure from institution-level asset managers who value stable, predictable margins.

The Order Book Versus Execution Quality

RVNL’s long-term strength has never been its lack of work—the company boasts a massive order book backlog running into tens of thousands of crores. The core issue exposed by the Q4 FY26 earnings is the quality and profitability of execution.

Moving forward, institutional investors will be monitoring the upcoming management commentary closely to answer crucial questions:

Were the Q4 margin compressions a temporary, one-off anomaly caused by specific project write-downs?

Are inflationary pressures permanently altering the cost landscape of current engineering, procurement, and construction (EPC) contracts?

What strategies is management deploying to restore operating margins back toward the healthier 6% to 7% territory?

Conclusion: A Turning Point for the Railway Giant

The latest corporate financial disclosure from Rail Vikas Nigam Limited marks a clear turning point in the company’s fiscal narrative. The RVNL Q4 results clearly indicate that while the company’s scale of operations remains massive and its top-line revenue continues a steady upward march, it is currently navigating a challenging operational environment.

The compression of its operating margins down to 4% and the resulting 58.9% decline in quarterly net profit serve as critical indicators for market participants. While the combined annual dividend distribution of ₹1.71 per share provides a modest cushion for income-focused portfolios, capital appreciation from these levels will rely heavily on management’s ability to control rising project costs and stabilize operating efficiency.

As the market digests these figures, the upcoming Annual General Meeting will be a critical event to watch. Investors will demand clarity on cost-management frameworks and guidance on whether the company can successfully transform its massive backlog into high-margin profits for the remainder of the fiscal year.

Disclaimer : Financial markets are subject to high risk. Please consult with a certified financial advisor before making any investment decisions.