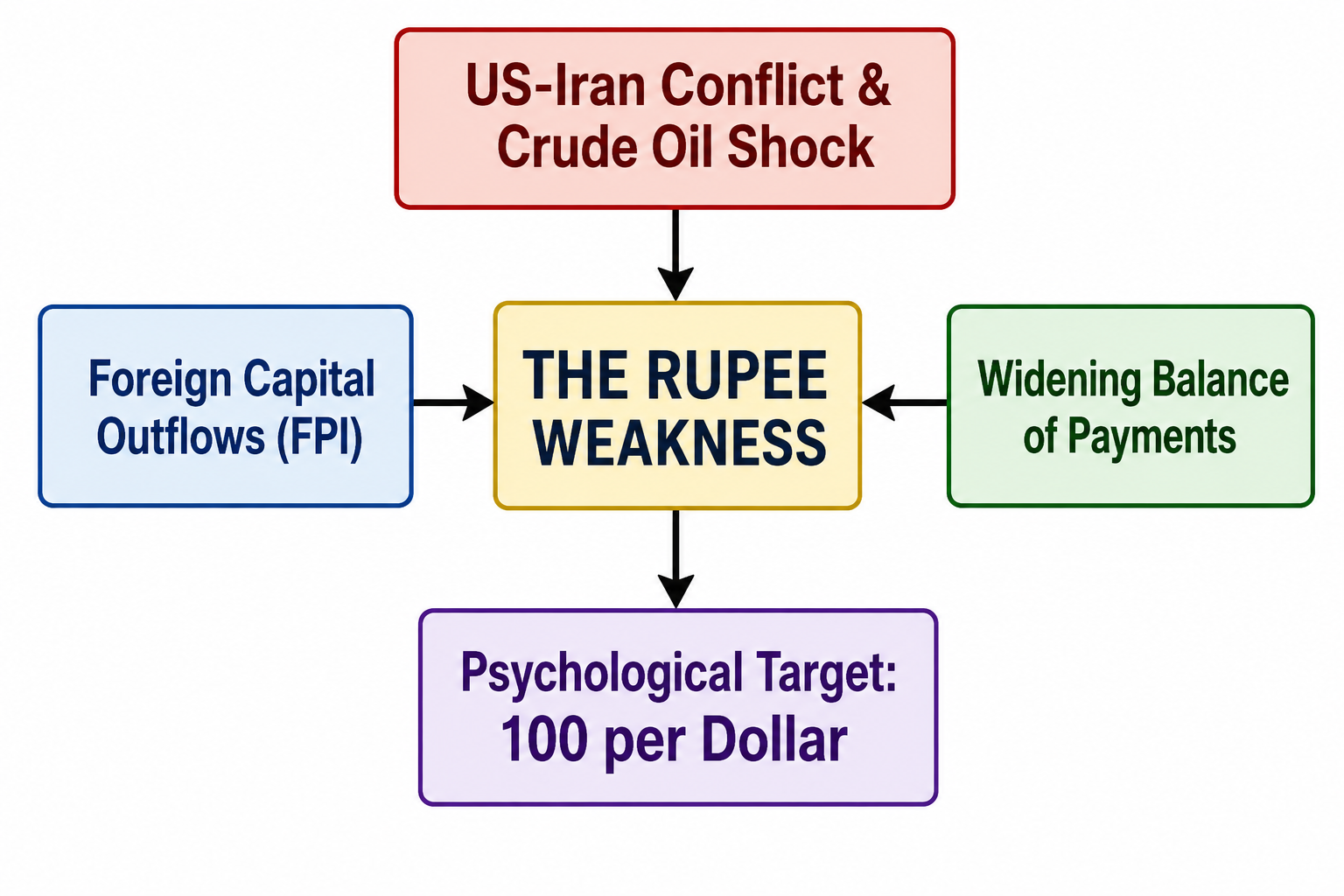

The Indian Rupee is facing an unprecedented storm in the global currency markets. Faced with escalating geopolitical conflicts, soaring crude oil import bills, and a massive exodus of foreign capital, global investors are positioning themselves for a sustained period of Rupee weakness. Many macro strategists and currency traders have begun actively gaming out scenarios where the Indian currency breaches the ultimate psychological barrier, sliding to an all-time low of 100 against the US Dollar.

As the local currency slides through critical support levels, the broader implications for India’s economic growth, domestic inflation, corporate profitability, and central bank monetary policy are coming under sharp scrutiny. Is this downward spiral a temporary market correction driven by external global shocks, or does it signal a deeper, structural crisis within India’s foreign direct investment framework?

The Perfect Storm: Why Global Funds Are Bearish on the Rupee

The fundamental pressures dragging down the Indian currency are multi-layered, combining sharp global geopolitical flare-ups with widening domestic economic imbalances.

1. The Geopolitical Crucible and Crude Oil Shock

The primary catalyst for the recent acceleration in currency depreciation is the ongoing conflict in the Middle East. Following a series of airstrikes involving regional powers and Western allies, global crude oil benchmarks have surged. Brent crude, which traded comfortably in the $70–$80 per barrel range earlier this year, has spiked past the $100 mark.

For an economy like India, which relies on foreign imports to satisfy over 85% of its domestic energy needs, this price shock is devastating. India consumes approximately 5.5 million barrels of crude oil every single day. When global energy prices scale upward, the math becomes punishing:

A mere $10 increase per barrel translates into an additional cash drain of $50 million every single day.

This constant requirement to purchase high-priced oil forces domestic entities to dump local currency and acquire US dollars, systematically undermining the exchange rate.

2. The Dominance of the US Dollar Greenback

As global geopolitical anxieties mount, international fund managers are executing a classic “flight to safety.” Investors are liquidating riskier emerging-market assets and parking their capital in safe-haven US dollar instruments. This structural preference for the greenback has triggered a comprehensive rally in the US Dollar Index, putting immense pressure on all major Asian currencies.

3. Rapid Erosion of Local Portfolio Gains

For international funds invested heavily in Indian equities and fixed-income instruments, sharp currency depreciation can instantly wipe out any localized market gains. If a foreign portfolio manager earns a 5% return on an Indian stock but the underlying currency loses 7% of its value against the dollar over the same period, the net investment return turns deeply negative when repatriated. This dynamic creates a vicious cycle: currency weakness triggers asset liquidations, and those very liquidations push the currency down further.

Market Forecasts: Revising the Levels

The rapid descent of the local unit has caught many market participants by surprise. After crashing through the 95 and 96 thresholds in quick succession, the currency recently touched an intra-day lifetime low of 96.81 per dollar, approaching the 97 mark. This represents a year-to-date drop of over 7%, far outpacing the 3% to 4% annual depreciation rate historically flagged as normal by policymakers.

In response, major banking conglomerates and institutional research desks have aggressively lowered their short-to-medium-term currency targets:

| Financial Institution | Revised Rupee Forecast Range (Per USD) | Previous Forecast Baseline |

| Kotak Mahindra Bank | 93.00 – 99.00 | 91.50 – 94.00 |

| ANZ Banking Group | 97.50 by Year-End | 93.00 |

| HSBC Holdings Plc | 95.50 | 93.50 |

| Gamma Asset Management | Tracking breach towards 100.00 | Bearish outlook maintained |

“The rupee remains vulnerable to further depreciation, and 100 against the dollar is an important psychological threshold that investors will increasingly focus on,” notes Rajeev De Mello, global macro portfolio manager at Gamma Asset. “The most immediate catalyst for a break of that level would be another leg higher in oil prices.”

Conversely, some contrarian institutions, such as the Amundi Investment Institute, suggest that after a broad-based regional selloff, Asian currencies are starting to look fundamentally undervalued. They argue that any de-escalation in global energy bottlenecks could pave the way for a sharp, structural appreciation surprise.

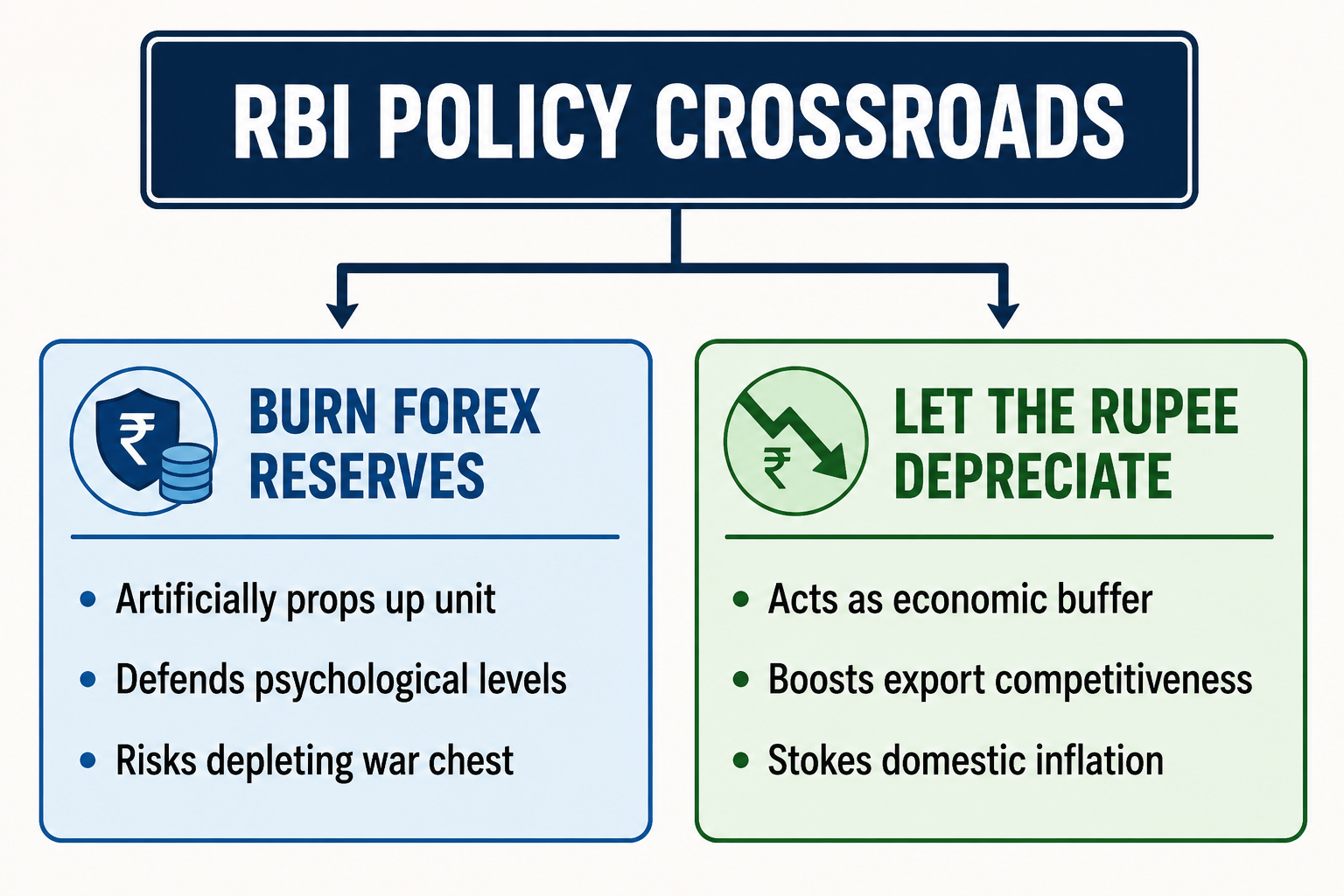

The Reserve Bank of India’s Dilemma: Intervention vs. Absorption

As the currency approaches historic thresholds, all eyes are on the Reserve Bank of India (RBI) and its massive foreign exchange war chest, which stands comfortably at $697 billion.

Historically, the central bank has maintained that it does not target a specific numerical level for the currency, choosing instead to step in exclusively to curb extreme, speculative volatility. However, the current macro framework presents a stark policy choice:

Allowing the Shock Absorber to Work: Prominent global economists, including Harvard professor and former IMF Deputy Managing Director Gita Gopinath, have argued that the central bank should avoid burning precious foreign exchange reserves to artificially defend the currency. In an environment dominated by external trade distortions, letting the currency find its market-determined equilibrium allows it to act as an automatic economic shock absorber.

The Export Silver Lining: A weaker domestic unit inherently reduces the price of local goods on the global market, boosting the structural competitiveness of textile, IT services, and pharmaceutical exports.

The Import Barrier: Conversely, a declining exchange rate increases the local cost of imported goods and foreign travel, acting as a natural, market-enforced austerity measure that dampens non-essential domestic demand for foreign luxury products.

Domestic Inflation and the Corporate ImpactWhile a weaker currency offers structural advantages to exporters, it presents immediate challenges for India’s domestic price stability and corporate earnings framework.

The Mechanism of Imported Inflation

Because India is a net importer, a falling exchange rate directly leads to imported inflation. When the local unit drops by 5% to 7% against the greenback, the landed cost of every critical item purchased from abroad—from advanced semiconductor microchips used in smartphones to industrial machinery and consumer goods—rises by that exact margin. This pricing pressure filters down into the consumer price index, threatening to destabilize retail inflation targets and compelling the central bank to keep domestic interest rates higher for longer.

Offsetting Corporate Fuel Relief

The intersection of currency depreciation and energy pricing is vividly illustrated in the performance of India’s public sector Oil Marketing Companies (OMCs). For an extended multi-month period, the domestic administration kept consumer fuel pump prices frozen to maintain retail stability during crucial state assembly elections. Following the conclusion of the polls, fuel prices were raised by approximately ₹3.90 per liter in consecutive installments to help OMCs recover lost margins.

However, analysis from SBI Research reveals that the rapid depreciation of the domestic currency has completely neutralized the benefits of these retail price hikes:

Every subsequent ₹2 drop in the exchange rate expands the effective landed cost of crude oil so sharply that it entirely consumes the margin relief generated by the ₹3.90 pump price hike. Consequently, industrial energy inputs remain elevated, threatening to trim corporate operating profits across manufacturing sectors.

The Broader Crisis: Tracking Capital Flight and Structural FDI Friction

Beyond temporary geopolitical triggers and energy price spikes, the relentless downward path of the currency is exposing a much more significant challenge: a structural shift in both foreign and domestic capital deployment.

1. The FPI Capital Flight

The balance of payments (BoP) functions as the definitive ledger of an economy’s financial relationship with the rest of the world. It is divided into the current account (tracking trade in physical goods and services) and the capital account (tracking the cross-border movement of investment funds).

While India has traditionally run a structural current account deficit due to its energy imports, this was historically balanced out by a strong surplus in the capital account. Today, that equation is shifting. In the early months of 2026 alone, Foreign Portfolio Investors (FPIs) pulled a record $23 billion from domestic equities, while injecting a modest $1.3 billion into local index-eligible debt instruments. On a net basis, global funds have pulled $22.4 billion out of the financial ecosystem this year. If this structural trend persists, it risks pushing India’s overall balance of payments into negative territory for a third consecutive year.

GLOBAL FUNDS MOVEMENT (YTD 2026)

┌────────────────────────────────────────────────────────┐

│ [████████████████████████████████████████] -$23B │ Equities Outflow

│ [█] +$1.3B │ Debt Inflow

└────────────────────────────────────────────────────────┘

Market analysts point out that international asset managers are reassessing their allocations due to a perception that certain sectors of the Indian equity market have become significantly overvalued. Concurrently, high-yielding fixed-income alternatives in developed markets offer attractive risk-adjusted returns without the accompanying emerging-market currency risk. Furthermore, veteran private equity (PE) firms that entered the domestic ecosystem five to seven years ago have reached the end of their investment lifecycles, leading to scheduled, large-scale profit repatriation out of the country.

2. Domestic Corporate Outward Investment

It is not merely international funds that are moving capital across borders; prominent domestic corporate houses are also investing heavily in overseas assets. Indian enterprises are currently deploying between $30 billion and $35 billion annually into offshore markets.

While a portion of this capital represents strategic acquisitions and the expansion of international subsidiaries, business analysts suggest it also reflects a tactical diversification strategy. Corporate leaders, observing a temporary softening in domestic rural consumption growth, are proactively deploying capital into external markets to unlock fresh revenue streams. In response to this trend, the central bank has scaled up its regulatory scrutiny of outbound direct investments, ensuring that capital transfers are tied strictly to bona fide operating businesses rather than speculative safe havens.

3. The 2017 Regulatory Framework Debate

The ongoing slowdown in fresh, inbound Foreign Direct Investment (FDI) has sparked intense debate among economic policymakers and academic experts. Independent data indicates that net FDI inflows into India have hovered close to zero for an extended period, raising questions about long-term structural attractiveness.

Prominent economists, including former members of the Prime Minister’s Economic Advisory Council, trace the roots of this slowdown back to sweeping legislative modifications enacted in 2017.

The 2017 Policy Shift Explained

Before 2017 (High Investor Comfort): If a dispute arose, global investors could take the matter directly to neutral, international courts. This gave them a high level of confidence to invest billions of dollars safely.

After 2017 (High Investor Anxiety): The government changed the rules, terminating old treaties. Now, foreign companies must litigate their disputes in domestic Indian courts first before they can ever look for international arbitration.

During that period, the administration moved to terminate existing Bilateral Investment Treaties (BITs), introducing a revised policy framework that mandates all investment disputes must be fully litigated through the domestic judicial system before seeking international, third-party arbitration.

For large global institutions managing billions of dollars, this requirement introduces considerable anxiety. Given the extended timelines, systemic backlogs, and complex procedural delays typical of the domestic legal ecosystem, international funds are displaying increased hesitation. Global capital prefers operating in environments with rapid, highly predictable dispute resolution mechanisms. Until these structural legal frictions are resolved, foreign corporate entities may continue to exercise caution, regardless of the country’s underlying consumption potential.

Strategic Outlook: Navigating the New Normal

The Indian currency is operating in a transformed global macroeconomic landscape. The combination of structural shift in global asset preferences, geopolitical energy distortions, and domestic regulatory frameworks means that a return to older currency baselines is unlikely in the short term.

To successfully navigate this period of Rupee weakness, a coordinated and comprehensive policy response is essential:

Energy Demand Management: Policymakers have urged citizens to adopt conscious fuel conservation strategies, optimize domestic energy consumption, and curb speculative gold purchases. Minimizing non-essential dollar outflows is a critical first line of defense against external account imbalances.

Accelerating Structural Reforms: Addressing the underlying concerns of global investors requires a clear look at regulatory frameworks. Revisiting the dispute resolution mechanisms in investment treaties and simplifying domestic production laws could help restore steady, non-speculative FDI inflows.

Enhancing Export Ecosystems: Rather than focusing purely on defending a specific currency level, domestic enterprises must capitalize on the enhanced competitiveness provided by a weaker exchange rate. Expanding logistics infrastructure and scaling up high-value manufacturing can help turn currency depreciation into an engine for export-led growth.

Ultimately, the currency market is behaving exactly as an open financial market should—reflecting real-time global risks, capital flows, and policy incentives. The current market signals offer a valuable window of opportunity. By prioritizing comprehensive economic reforms over short-term political debates, India can strengthen its structural fundamentals, transforming current market volatility into a foundation for resilient, long-term global economic integration.

Disclaimer: This information is based on various inputs from news agency